Stanford Machine Learning Notes

Info

Introduciton

What is machine learning

- Arthur Samuel (1959): Field of study of that gives computers the ability to learn without being explicitly programmed.

- Tom Mitchel (1998): A Well-posed Learning Problem is *A computer program is said to learn from experience E with repsect to some task T and some performance measure P, if its performance on T, as measured by P, improves with experience E.

Machine learning algorithms:

We mainly talks about two types of algorithm:

- Supervised Learning

- Unsupervised Learning

- Others: Reinforcement Learning, Recommender System.

And Practical advice for applying learning algorithm

Supervised Learning

"Right Answers" are given.

Linear Regression (Week 1)

Model Representation

Notations:

- \(m\) is Number of training examples.

- \(x\)'s is "input" variable / feature.

- \(y\)'s is "output" variable / "target" variables.

- \((x,y)\) is one training example.

- \((x^{(i)},y^{(i)})\) is the \(i\)th example, \(i\) starts from \(0\).

- \(h\) is called hypothesis, it maps the input to output. In this lecture, we represent \(h\) using linear function, thus it's called linear regression. For linear regression with one variable, it's called univariate linear regression. For example, the univariate linear regression is usually written as: \(h_\theta (x) = \theta_0 + \theta_1 x\). The \(\theta\) here represents the coefficient variables. Sometimes it's written as \(h(x)\) as a shorthand.

Cost Function

Since the hypothesis is written as \(h_\theta (x) = \theta_0 + \theta_1 x\), where \(\theta_i\)'s are the parameters, then how to choose \(\theta_i\)'s? The idea is to choose \(\theta_0, \theta_1\) so that \(h_\theta (x)\) is close to \(y\) for our training examples \((x,y)\). More formally, we want to \[ \underset{\theta_0,\theta_1}{\text{minimize}} \frac{1}{2m}\sum_{i=1}^{m}\left( h_\theta(x^{(i)}) - y^{(i)} \right)^2 \], where \(m\) is the number of trainnig examples. To recap, we're minimizing half of the averaging error. Note that the variable here are \(\theta\)s, and \(x\) and \(y\)'s are constants.

By convention, we define the cost function \(J(\theta_0,\theta_1)\) to represent the objective function. That is

\begin{gather*} J(\theta_0,\theta_1) = \frac{1}{2m}\sum_{i=1}^{m}\left( h_\theta(x^{(i)}) - y^{(i)} \right)^2 \\ \underset{\theta_0,\theta_1}{\text{minimize}} J(\theta_0,\theta_1) \end{gather*}This cost function is also called squared error function. There are other cost functions, but it turns out that squared error function is a resonable choice and will work for most of regression problem.

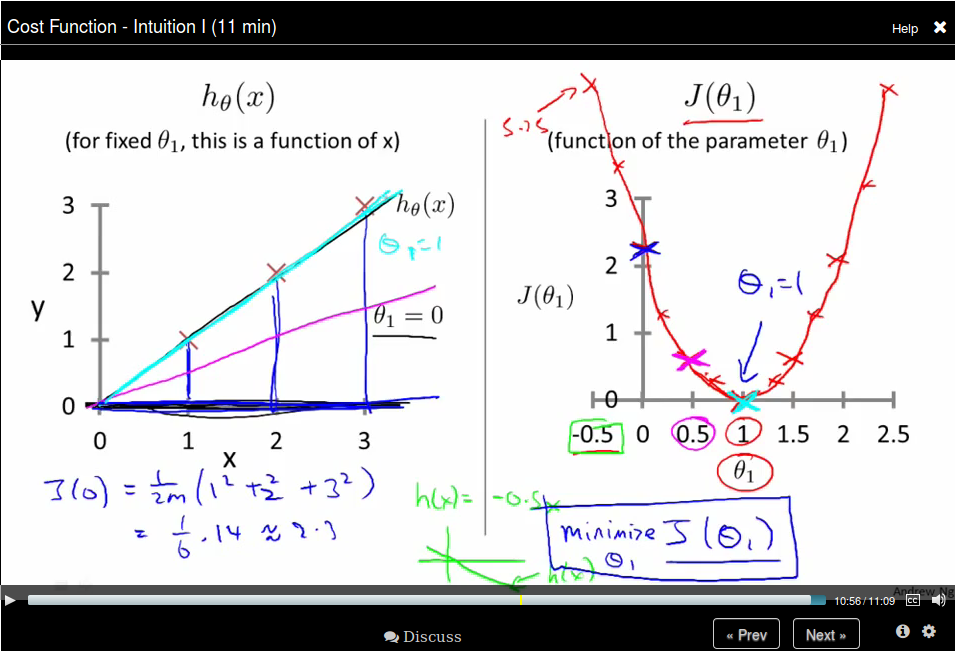

Cost Function Intuition

Before getting a intuition about the cost function, let's have a recap, we now have

- Hypothesis: \[h_\theta (x) = \theta_0 + \theta_1 x\]

- Parameters: \[\theta_0,\theta_1\]

- Cost Function: \[J(\theta_0,\theta_1) = \frac{1}{2m}\sum_{i=1}^{m}\left( h_\theta(x^{(i)}) - y^{(i)} \right)^2 \]

- Goal: \[\underset{\theta_0,\theta_1}{\text{minimize}} J(\theta_0,\theta_1)\]

In order to visualize our cost function, we use a simplified hypothesis function: \(h_\theta (x) = \theta_1 x\), which sets \(\theta_0\) to \(0\). So now we have

- Hypothesis: \[h_\theta (x) = \theta_1 x\]

- Parameters: \[\theta_1\]

- Cost Function: \[J(\theta_1) = \frac{1}{2m}\sum_{i=1}^{m}\left( h_\theta(x^{(i)}) - y^{(i)} \right)^2 \]

- Goal: \[\underset{\theta_1}{\text{minimize}} J(\theta_1)\]

So now let's compare function \(h_\theta (x)\) and function \(J(\theta_1)\):

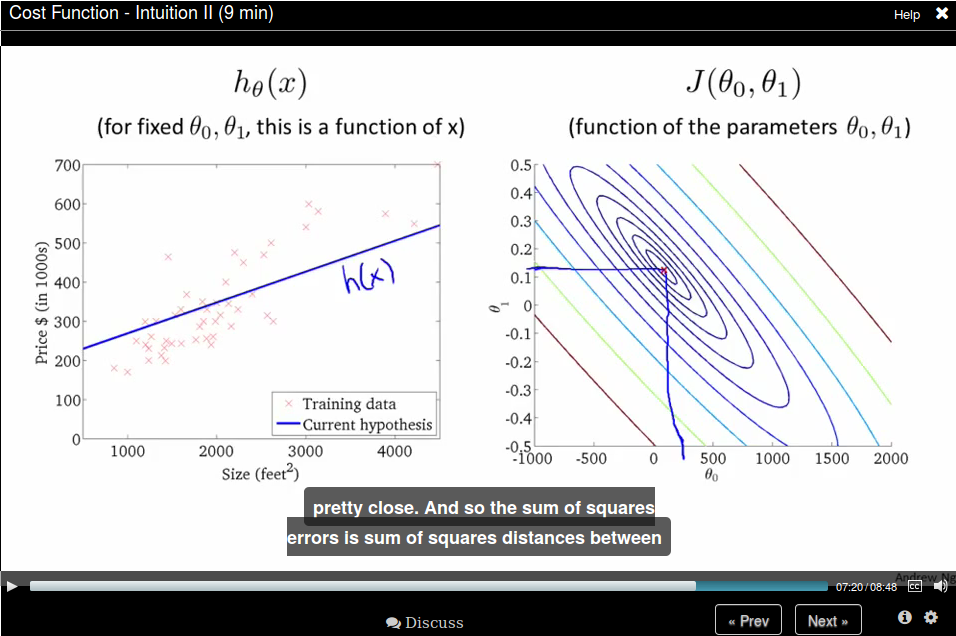

Then let's come back to the original function, where we don't have the constrain that \(\theta_0 = 0\). The comparison is like

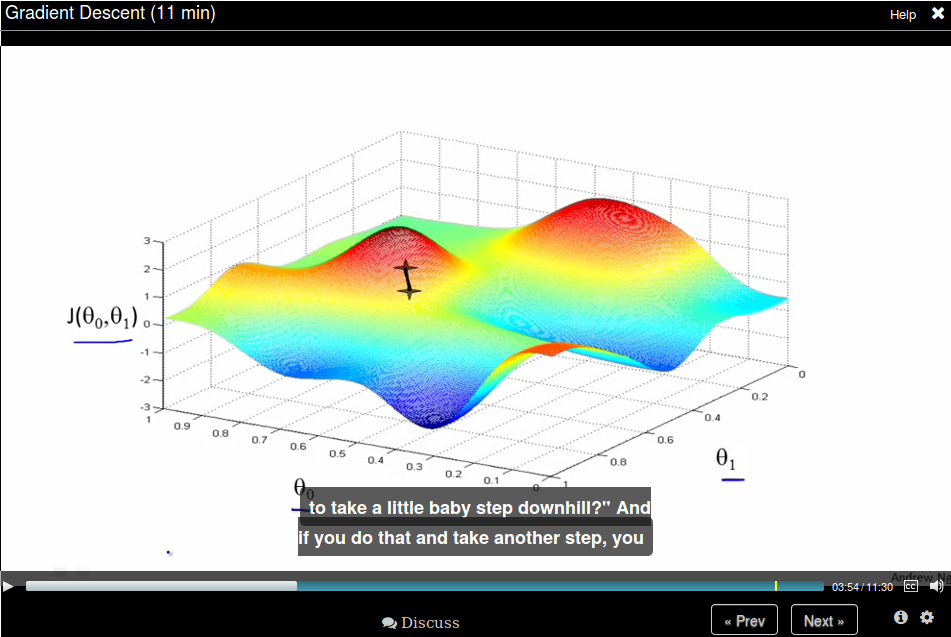

Gradient Descent

Now we have some function \(J(\theta_0,\theta_1)\) and we want to \(\underset{\theta_0,\theta_1}{\text{minimize}}J(\theta_0,\theta_1)\), we use gradient descent here, which

- Start with some \(\theta_0,\theta_1\),

- Keep changing \(\theta_0,\theta_1\) to reduce \(J(\theta_0,\theta_1)\), until we hopefully end up at a minimum.

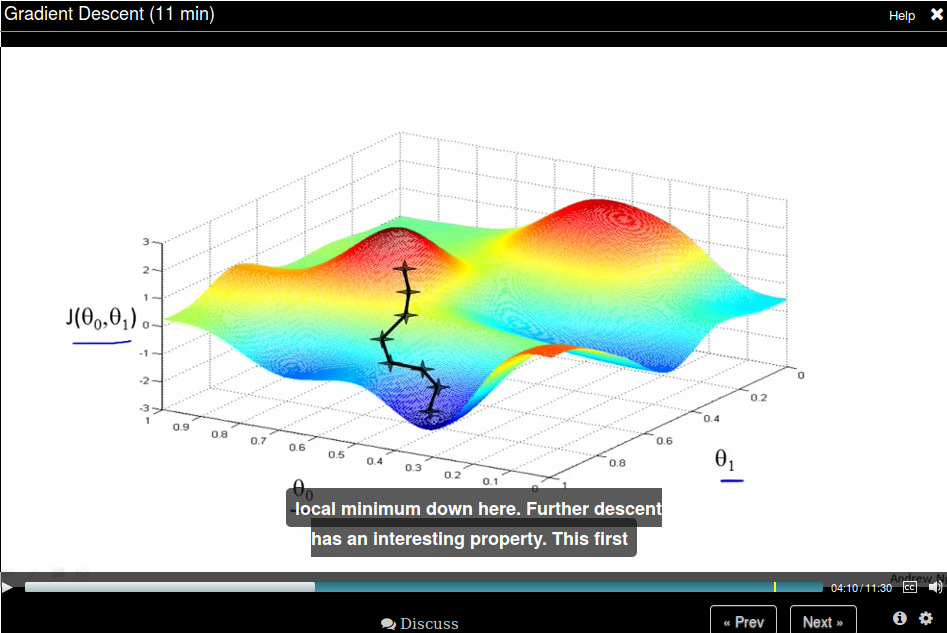

To help understand gradient descent, suppose you are standing at one point on the hill, and you want to take a small step to step downhill as quickly as possible, then you would choose the deepest direction to downhill.

You keep doing this until to get to a local minimum.

You keep doing this until to get to a local minimum.

But if you start with a different initial position, gradient descent will take you to a (very) different position.

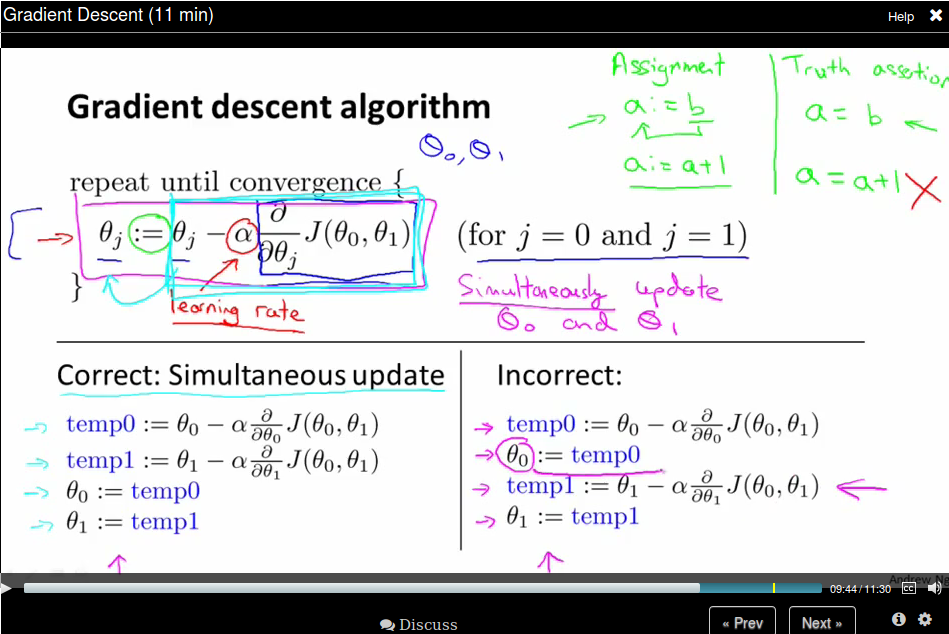

Gradient Descent algorithm

We use \(a := b\) to represent assignment and \( a = b\) to represent truth assertion.

The \(\alpha\) here is called learning rate.

Pay attention that when implementing gradient descent, we need to update all \(\theta\text{s}\) simultaneous.

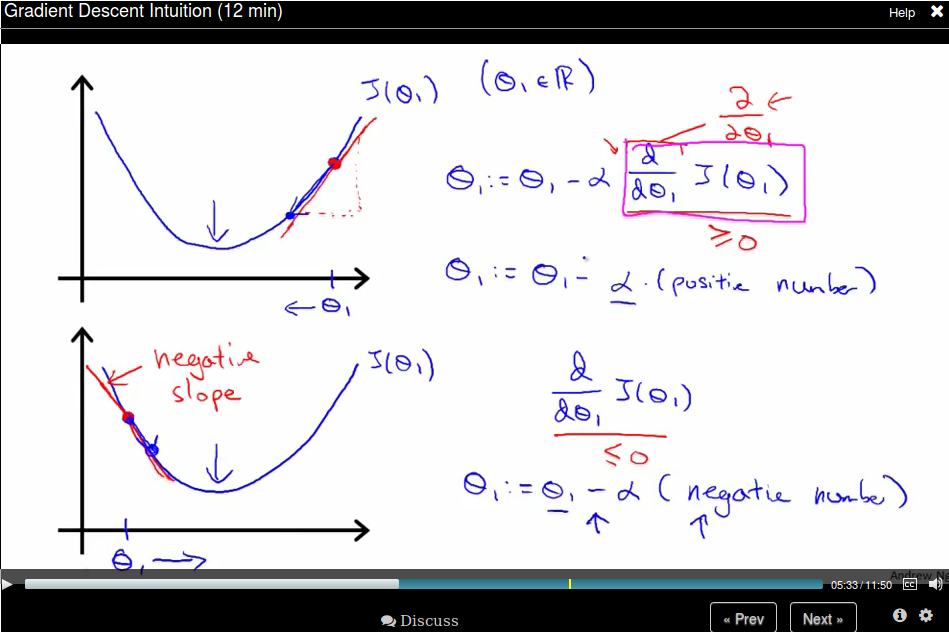

Recall that \(\alpha\) is a called the learning rate, which is actually a scale factor to our step represented by the derivative term. Take a 1D case as an example, the derivative is the direction (slop of the tanget line) where the function value becomes larger, so we should take its negative as our step.

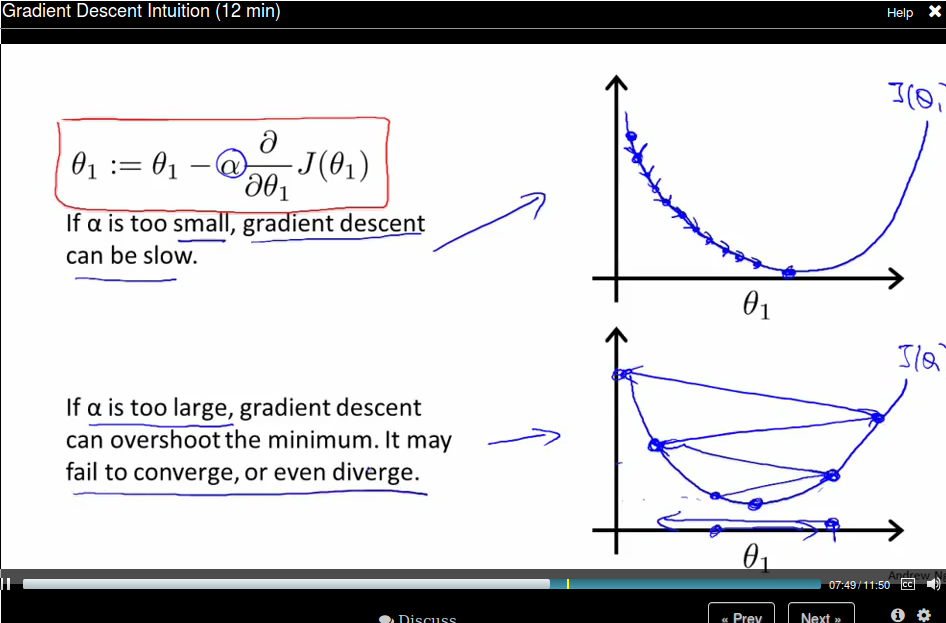

If \(\alpha\) is too small, gradient descent can be slow. If \(\alpha\) is too large, gradient can overshoot the minimum. It may fail to converge, or even diverge.

Gradient descent can converge to a local minimum, even with the learning rate \(\alpha\) fixed. This is because as we approach a local minimum, gradient descent will automatically take smaller steps. So no need to descrease \(\alpha\) over time.

Batch Gradient descent: Each step of gradient descent uses all the training examples:

Linear Algebra (Week1, Optional)

This lecture use 1-indexed subscripts.

Linear Regression with Multiple Variables (Week 2)

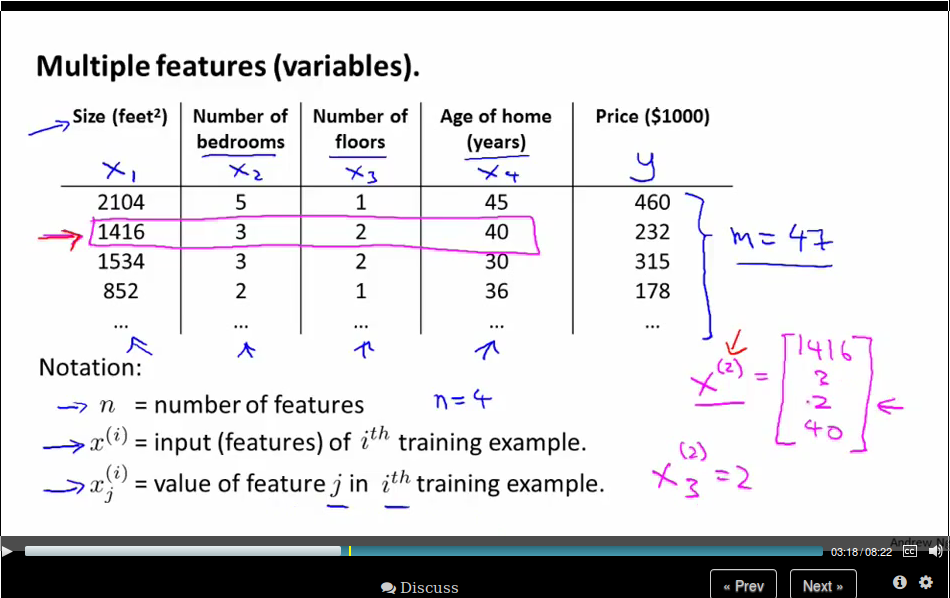

Multiple Features

Notation:

Notation:

- number of features: \(n\)

- input (features) of \(i^{\text{th}}\) training example: \(x^{(i)}\)

- value of feature \(j\) in \(i^{th}\) training example. \(x^{(i)}_{j}\)

Now our hypothesis is \(h_\theta (x) = \theta_0 + \theta_1 x_1 + \theta_2 x_2 + \dots + \theta_n x_n \). For convenience of notation, define \(x_0 = 1\), or \(x^{(i)}_0 = 1\). So now we define our hypothesis as

\begin{equation*} \begin{split} h_\theta (x) &= \theta_0 x_0 + \theta_1 x_1 + \theta_2 x_2 + \dots + \theta_n x_n \\ &= \theta x \end{split} \end{equation*}where \(\theta\) is a \(n+1\) dimension vector.

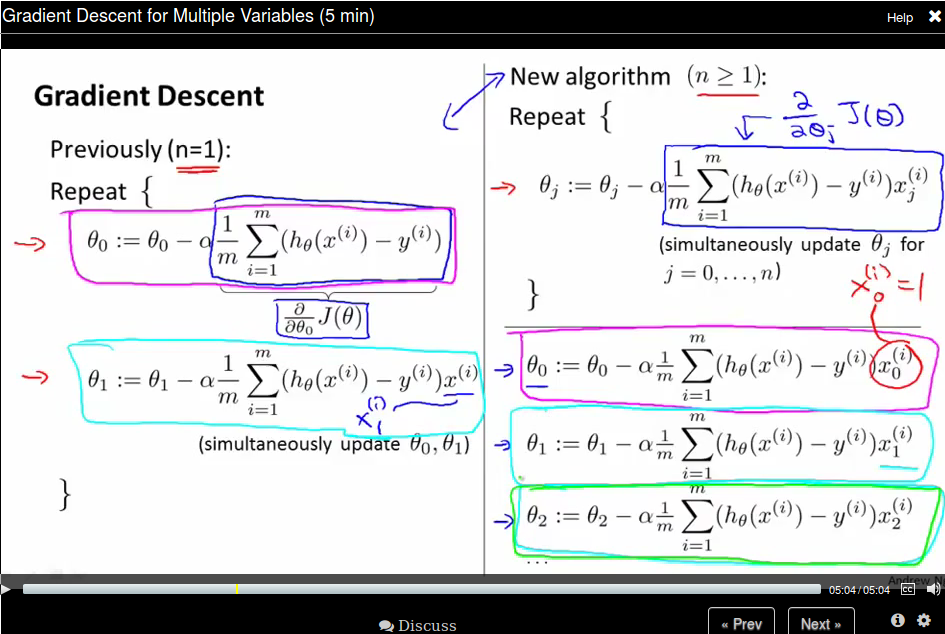

Gradient Descent for Multiple Variables

So now our new algorithm becomes

Note that our new algorithm for \(\theta_0\) is just like the old one since \(x_0^{(i)} \) is 1.

Note that our new algorithm for \(\theta_0\) is just like the old one since \(x_0^{(i)} \) is 1.

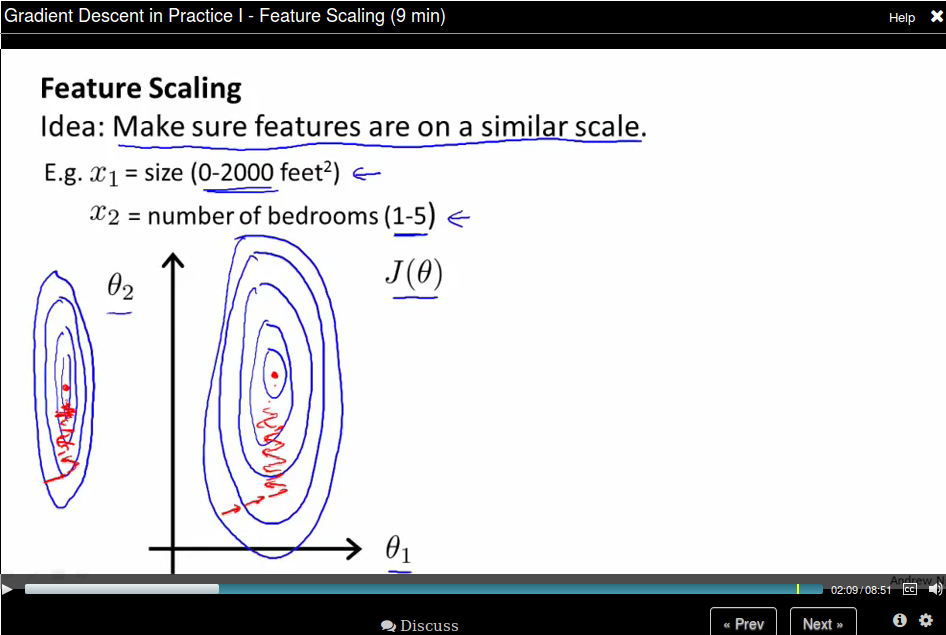

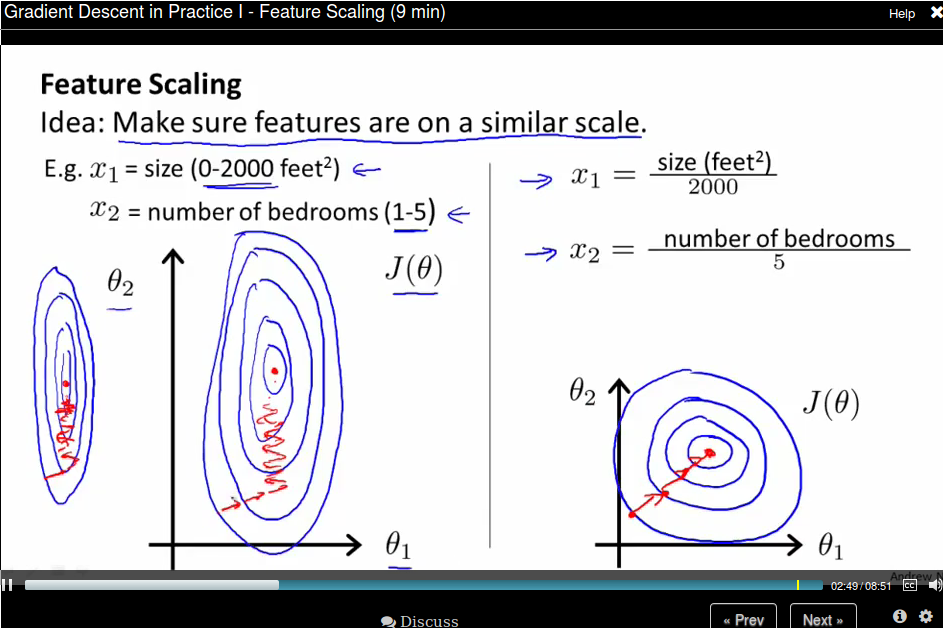

Gradient Descent in Practice - Feature Scaling.

Idea: Make sure features are on a similar scale, then gradient descent will converge more quickly.

Take a 2D example, if the dimension of \(x_1\) is much larger than the dimension of \(x_2\), then the search region is a long ellipsis shape which is make gradient much difficult to find the minimum.

We can rescale all features to [0,1] so the contours now become a circle.

We can rescale all features to [0,1] so the contours now become a circle.

Usually we get every feature into approximately a \(-1 \leq x \leq 1\) range. But it need not to be exactly. Say \(-3 \leq x \leq 3 \) is OK.

Mean normalization: Replace \(x_i\) with \(x_i - \mu_i\) to make features have approximately zero mean. Note that this does not apply to \(x_0 = 1\).

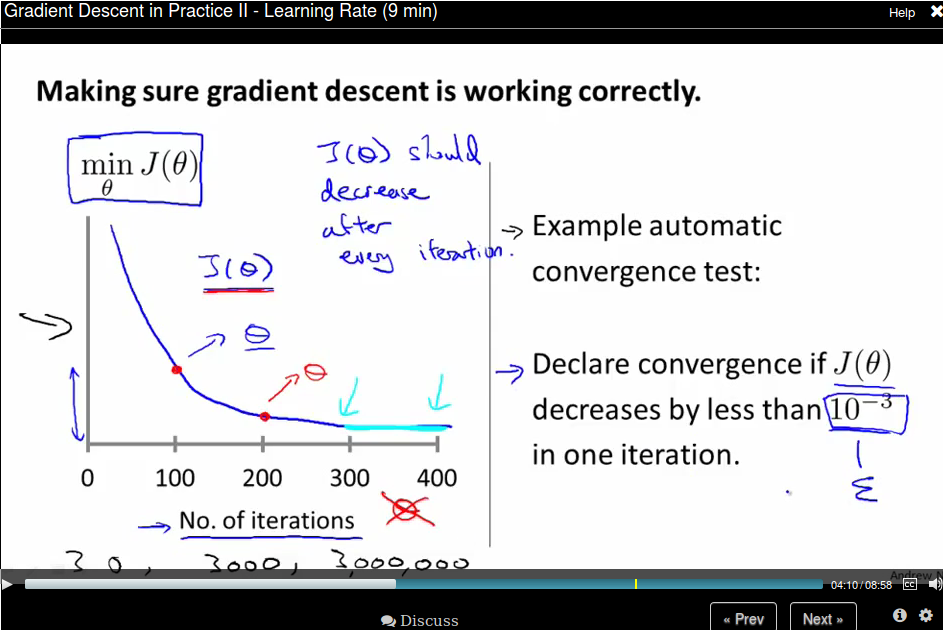

Gradient Descent in Practice - Learning Rate.

To make sure gradient descent is working correctly, draw the figure the value of \(J(\theta)\) versus the number of iterations.

For sufficiently small \(\alpha\), \(J(\theta\) should decrease on every iteration. But if \(\alpha\) is too small, gradient descent can converge too slow. To choose \(\alpha\) try \( \dots, 0.001, 0.003,0.01, 0.03,0.1, 0.3,1, \dots\), roughly a 3x larger.

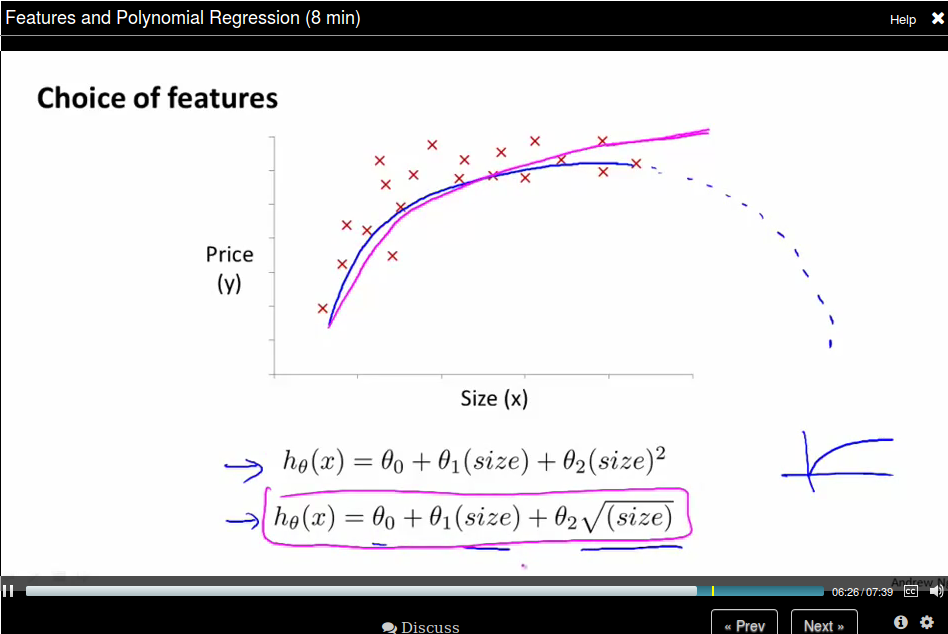

Features and Polynomial Regression

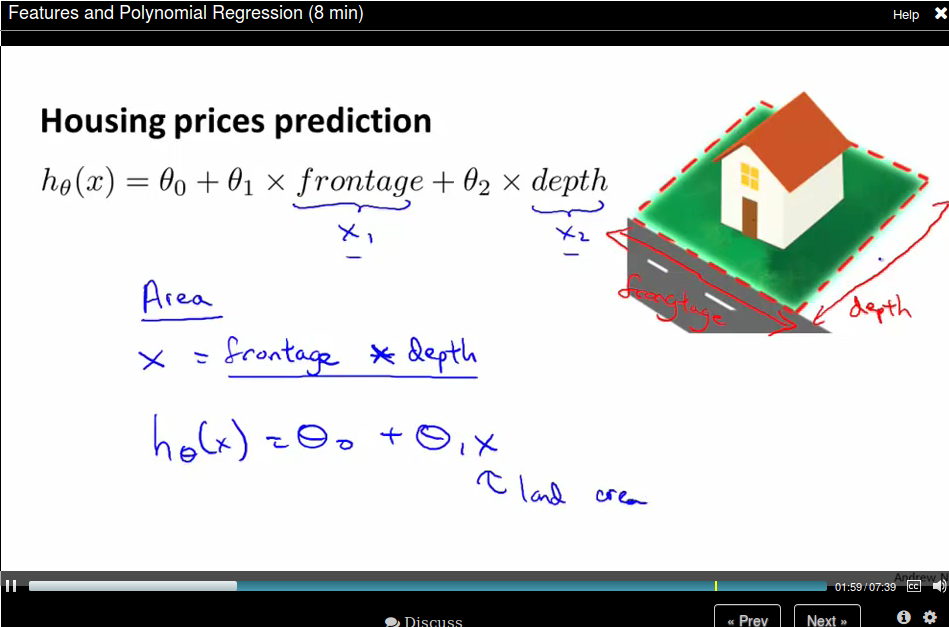

You need to choose a good feature instead of just using what you're provided. For example, for housing price prediction, you are provided with the frontage and depth feature, you can define a feature called area = frontage x depth.

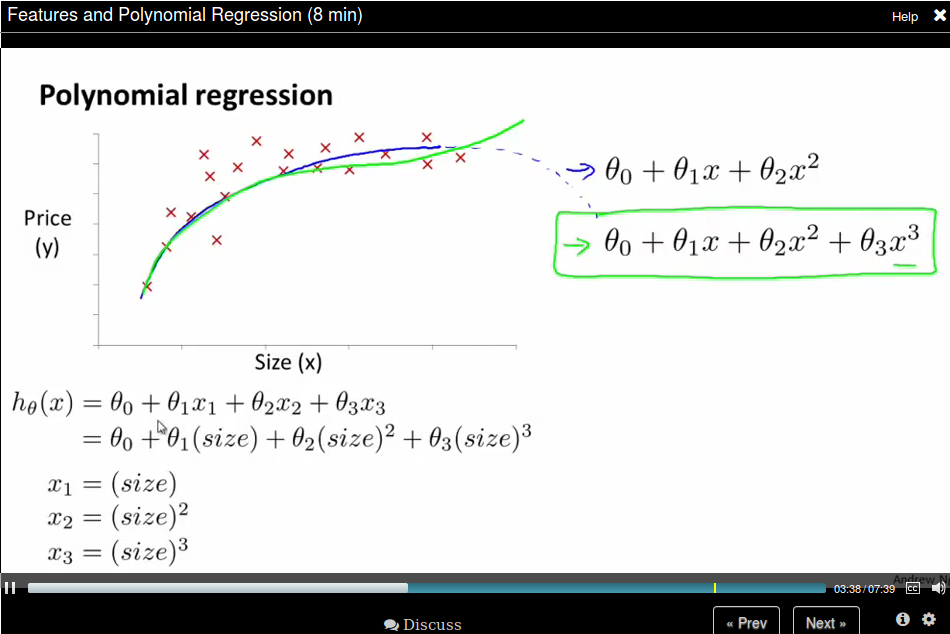

Or sometimes use a polynomial function would be better. If the feature is not enough, you could use size, size^2, size^3 as features.

Or you can use square root as feature.

How to find the minimum of \(J(\theta)\) analytically?

How to find the minimum of \(J(\theta)\) analytically?

By Calculus, we can take the partial derivatives of each variable, and set it to 0.

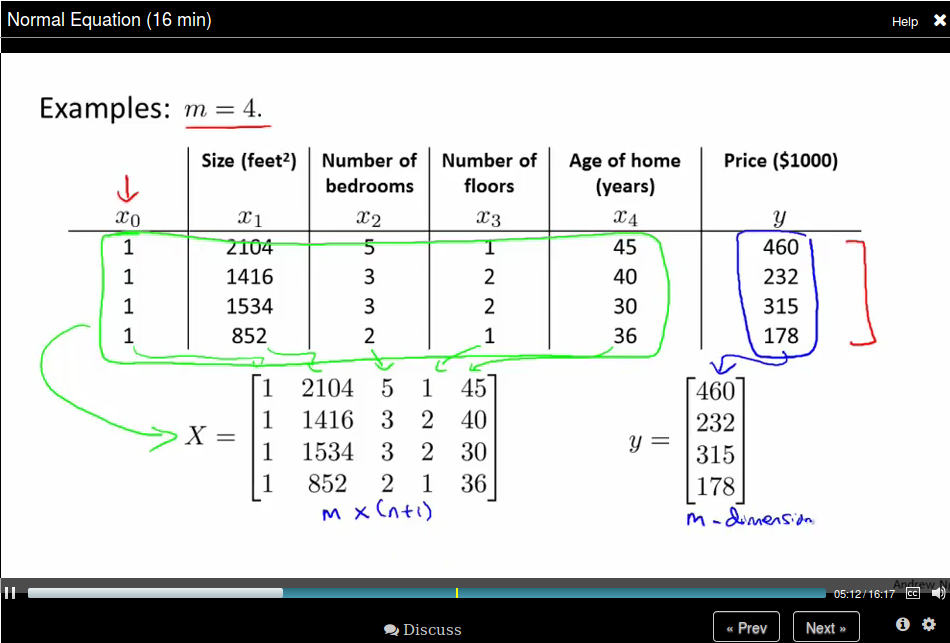

Normal Equation:

Then we can compute \(\theta = (X^T X)^{-1} X^T y\)

The Octave code is:

Then we can compute \(\theta = (X^T X)^{-1} X^T y\)

The Octave code is:

pinv(X' * X) * X' * y

Compare Gradient Descent with Normal Equation.

Normal Equation and Noninvertbility (Optional)

Use pinv in Octave should not be a problem.

What if \(X^T X\) is non-invertible?

- Reduent features (linearyly dependant). E.g. \(x_1\) = size in feet, \(x_2\) size in m^2.

- Too many features (e.g. $m ≤ n). Delete some features, or use regulariation.

Octave Tutorial

Basic Operation

5+6 3-2 5*8 1/2 2^6 1 == 2 %false 1 ~= 2 1 && 0 1 || 0 xor(1,0) %XOR PS1('>> '); % to change the prompt sign a = 3; % semicolon supressing output a disp(a); disp(sprintf('2 decimals: %0.2f', a)) a format long a format short a A = [1 2; 3 4; 5 6] A = [1 2 3 4 5 6] v = [1 2 3] v = 1:0.1:2 ones(2,3) C = 2*ones(2,3) C = [2 2 2; 2 2 2] w = ones(1,3) w = zeros(1,3) w = rand(1,3) rand(3,3) rand(3,3) w = randn(1,3) % guassian distribution w = -6 + sqrt(10)*(randn(1,10000)); % you don't want to omit the semicolon here hist(w) hist(w,50) eye(4) % identity matrix I = eye(6) help eye

Move data around

A = [1 2; 3 5; 5 6] size(A) sz = size(A) size(A,1) v = [1 2 3 4] length(v) length(A) length([1;2;3;4;5]) pwd cd .. ls load('test.dat') who whos save hello.mat v save hello.txt v -ascii clear A = [1 2 ; 3 4; 5 6]; A(3,2) A(:,2) A([1 3], :) A(:,2) = [10; 11; 12] A = [A, [ 100, 101, 102]]; A(:) % put all elements of A into a single vector A = [1 2; 3 4; 5 7]; B = [11 12; 13 14; 15 16]; C = [A B] C = [A,B] D = [A; B]

Computing on Data

A = [1 2; 3 4; 5 6]; B = [11 12; 13 14; 15 16]; C = [11 12; 13 14] A.*B A.^2 v = [1; 2; 3] 1 ./ v 1 ./ A log(v) exp(v) abs(v) abs([-1; 2; -3]) -v v + ones(length(v),1) v + 1 A' (A')' a = [1 15 2 0.5] val = max(a) [val, ind] = max(a) max(A) a < 3 A = magic(3) [r,c] = find(A >= 7) sum(a) prod(a) floor(a) ceil(a) max(A,[],1) % colomn wise max max(A,[],2) % row wise max max(A) max(max(A)) max(A(:)) % find max of all the elements A = magic(9) sum(A,1) % column wise sum sum(sum(A .* (eye(9)))) % sum the diagonal values sum(sum(A .*flipud(eye(9)))) % sum the subdiagonal values pinv(A) # sudo inverse temp = pinv(A) temp * A

Plotting Data

t = [0:0.01:0.98]; y1 = sin(2*pi*4*t); plot(t,y1); y2 = cos(2*pi*4*t); plot(t,y2); plot(t,y1); hold on; plot(t,y2,'r'); xlabel('time'); ylabel('value'); legend('sin','cos'); title('my plot'); print -dpng 'myPlot.png' close figure(1); plot(t,y1); figure(2); plot(t,y2); subplot(1,2,1)% divides plot into a 1x2 grid, access first element plot(t,y1); subplot(1,2,2); plot(t,y2); axis([0.5 1 -1 1]) % change horizontal range to [0.5,1] and vertical to [-1,1] A = magic(5) imagesc(A) imagesc(A), colorbar, colormap gray; % use comma for command chainning, for ouput, which is different from semicolon

Control Statements

v = zeros(10,1) for i = 1:10, v(i) = 2^i; end; i = 1; while i <= 5, v(i) = 100; end i = 1; while true, v(i) = 999; i = i + 1; if( i == 6), break; end; end;

Vectorizatrion

\(h_\theta(x) = \sum_{j=0}^{n} \theta_j x_j = \theta^T x\)

%unvectorized implemenetation predictaion = 0.0; for j = 1;n+1, prediction = prediction + theta(j) * x(j) end; %vectorized implementation prediction = thteta' * x;

Logistic Regression (Week 3)

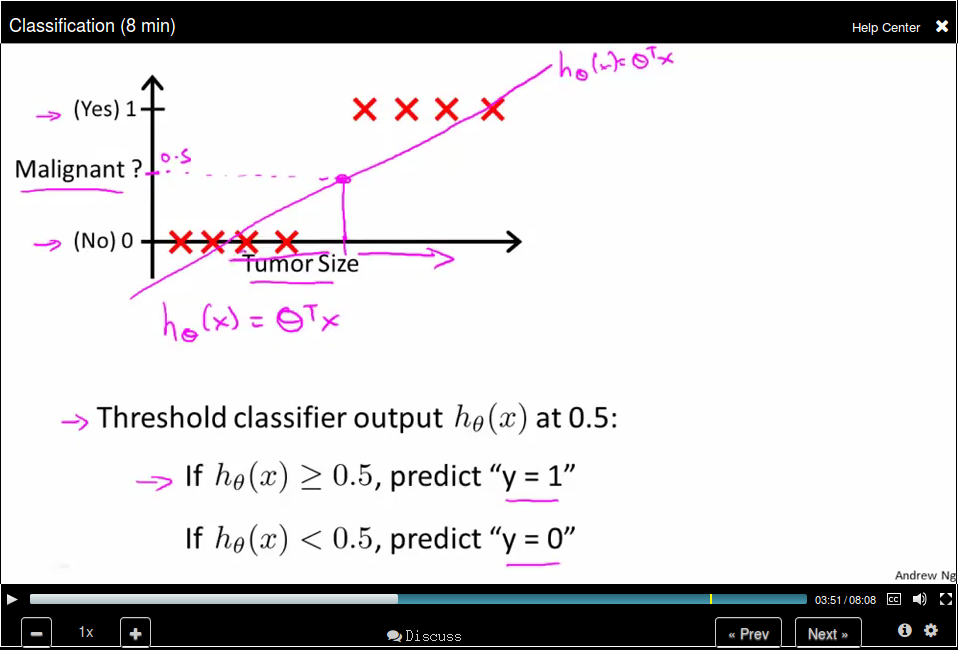

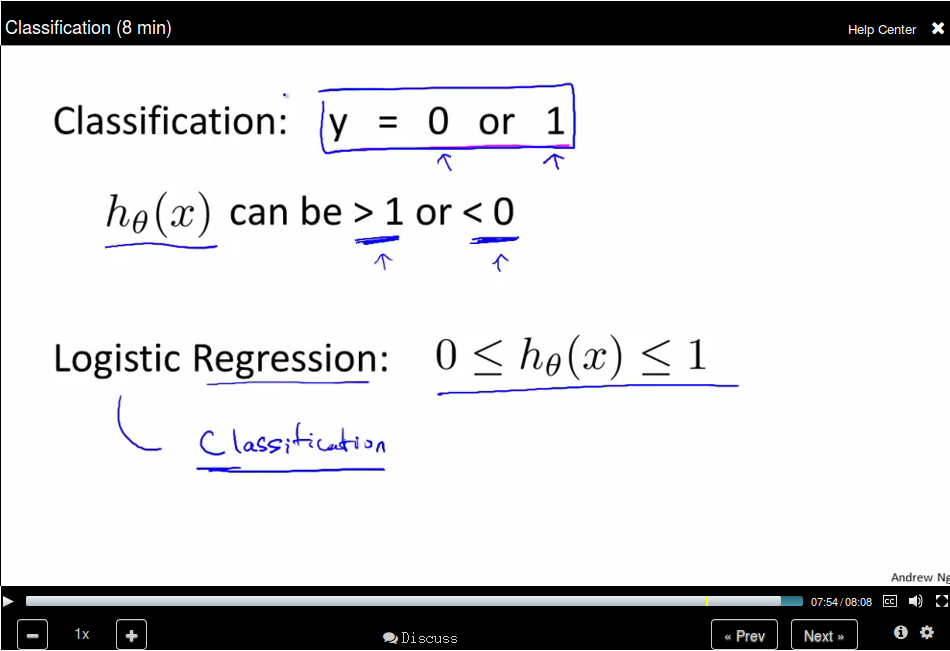

Classification (8min)

Applying linear regression to a classification problem is not a good idea.

You can use 0.5 as a threshhold to do the prediction based on the h_θ(x)

value. However, this is not a good idea since when adding a new sample point,

the hypothesis will change. Besides, the return value for h_θ(x) could be

not in the range [0, 1], thus making the prediction rather confusing. Logistic

Regression, though the word regression, is used to do the classification job and

the hypothesis can be guaranteed in the range [0,1].

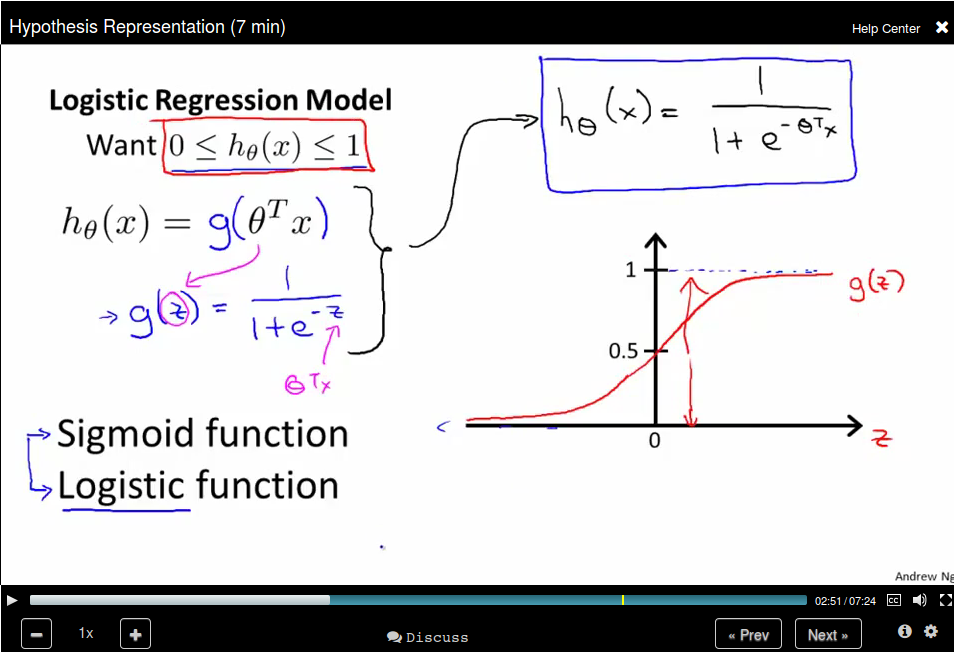

Hypothesis Representation

Logistic Regression Model

We set \(h_\theta(x) = g(\theta^Tx)\), where \(g(z) = \frac{1}{1+e^{-z}}\). The \(g\)

function is called Sigmoid function as well as Logistic function.

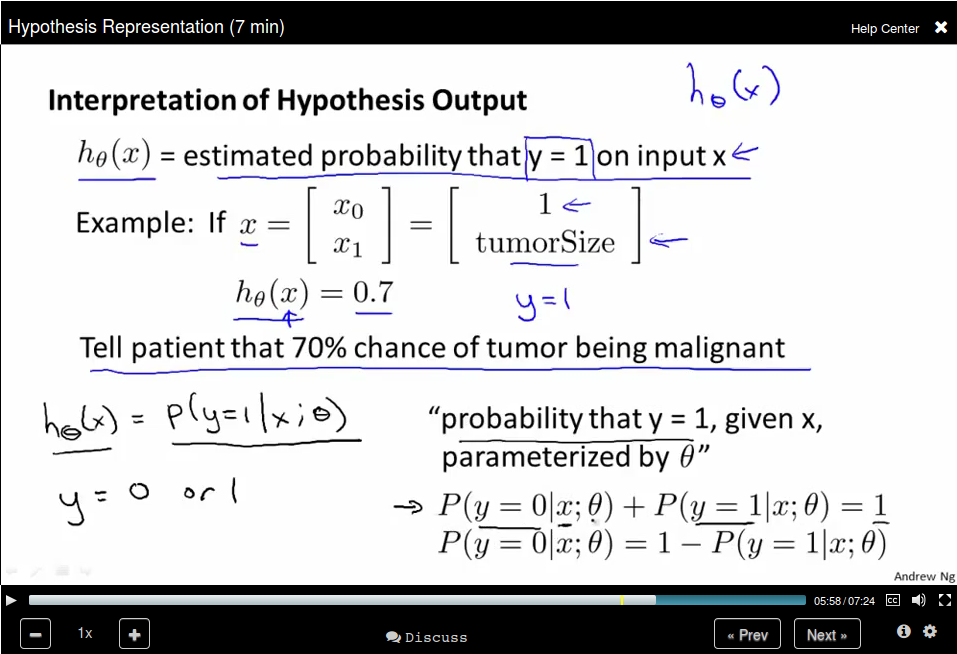

Interpretation of Hypothesis Output

You can think of \(h_\theta(x)\) as the estimated probability that \(y = 1\) on

input \(x\).

Decision Boundary

It's a line that separates the regions where the hypothesis predicts 1 or 0.

Since \(g(z) \geq 0.5\) when \(z \geq 0.5\), which means that \(h_\theta(x) \geq 0.5\) whenever \(\theta^{T} x \geq 0\)

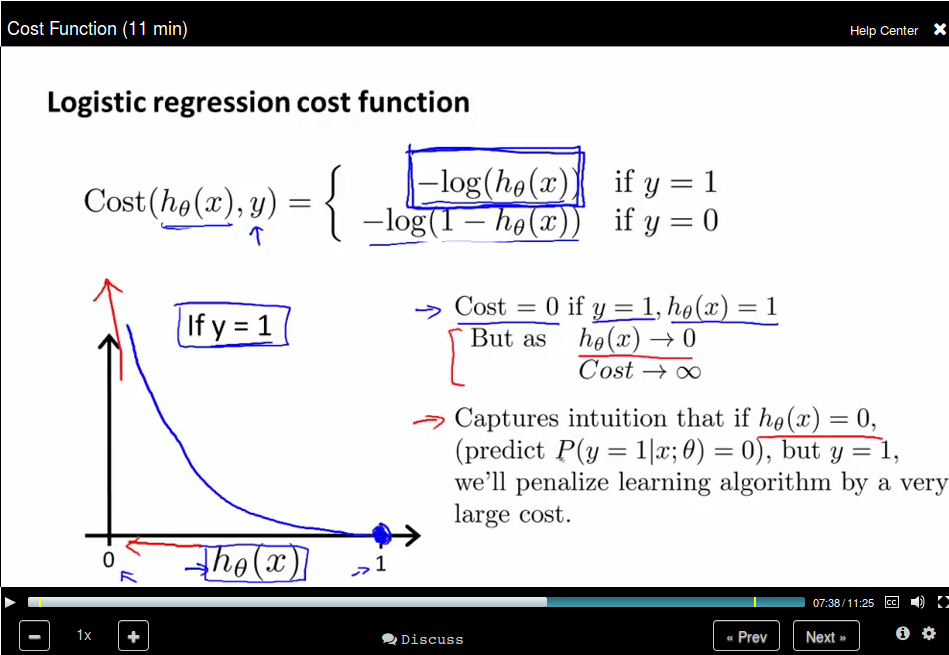

Cost Function

How to fit the parameters θ for Logistic Regression?

We define the cost function as below since \(h_\theta(x)\) is in the range [0,1].

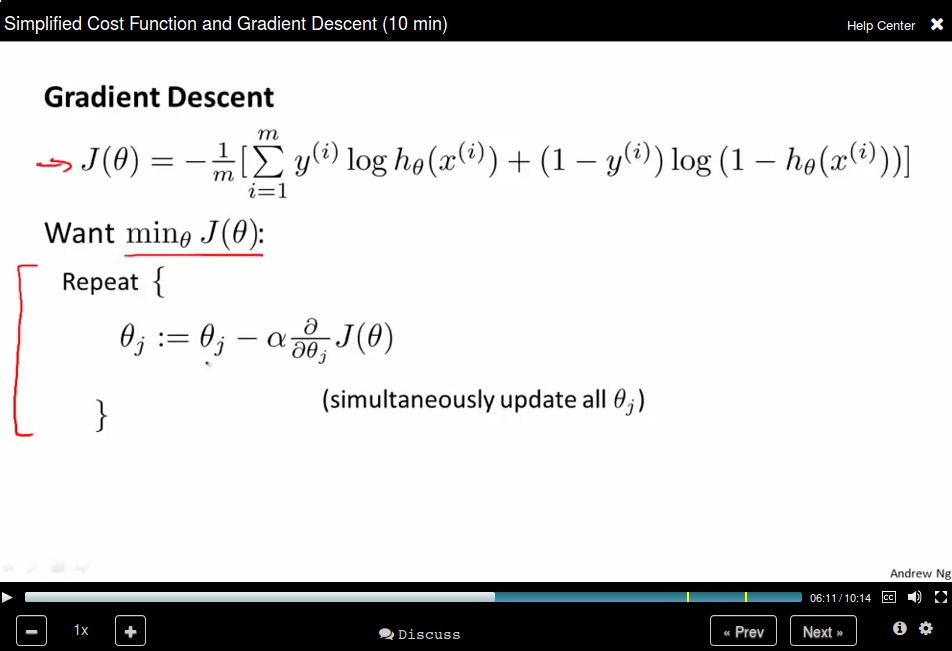

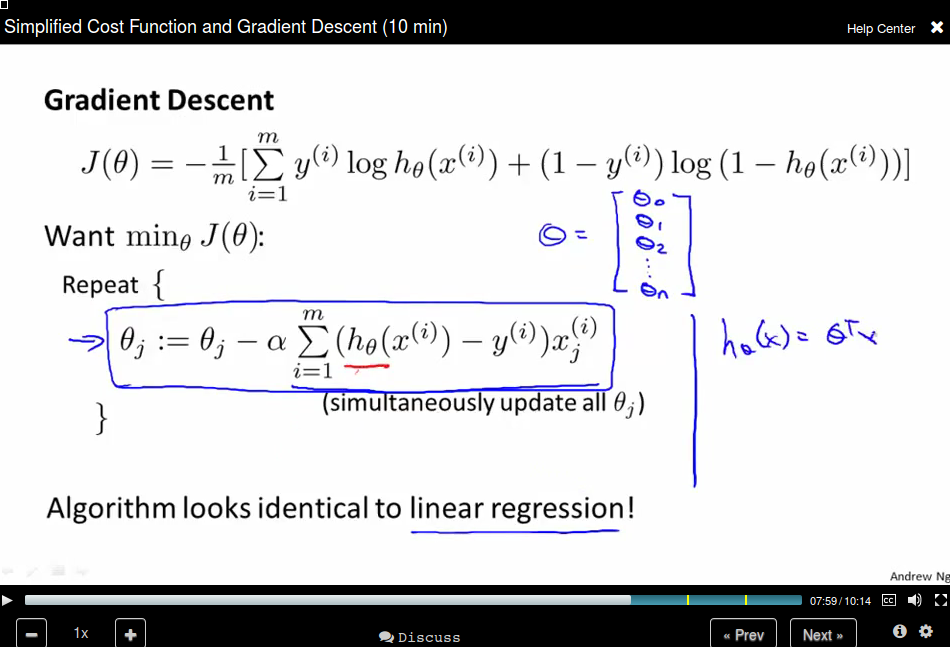

Simplified Cost Function and Gradient Descent

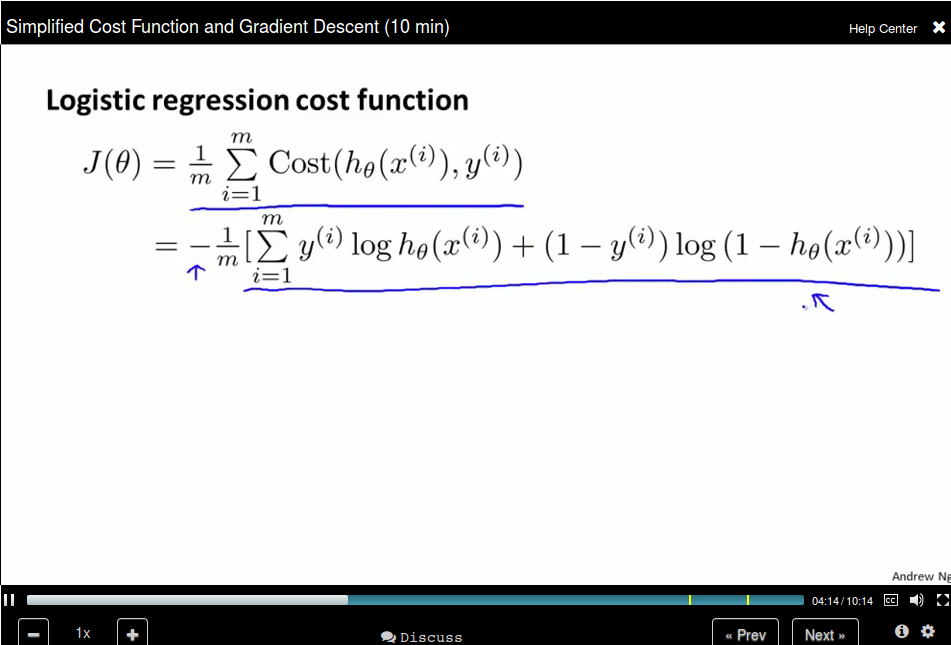

Remember that the Logistic regression cost function is in two parts, since y can be 0 or 1 only, we can write the cost function in a new way:

Remember that gradient descent is like:

where the partial derivatives is like:

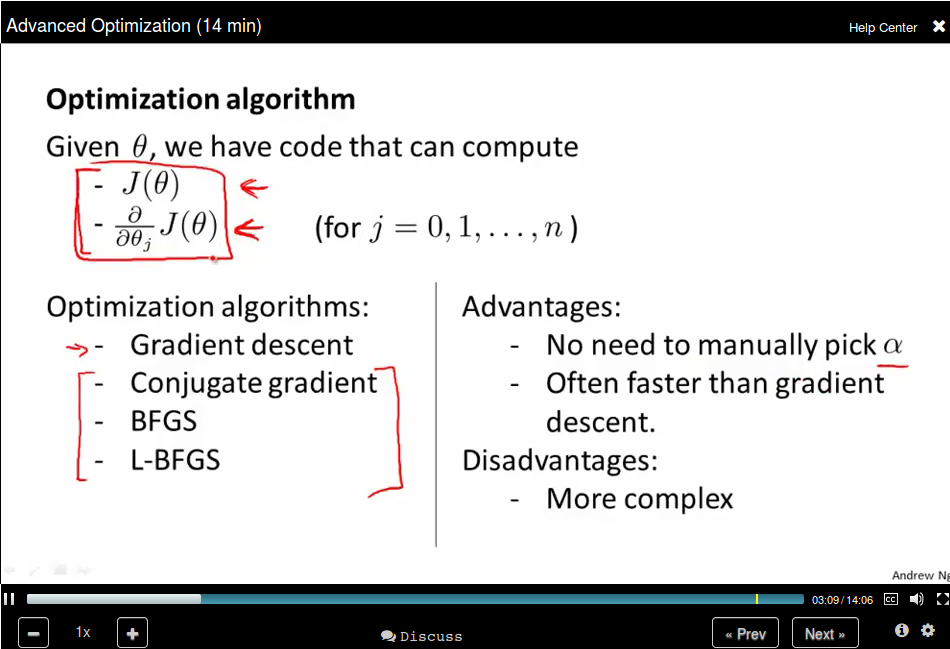

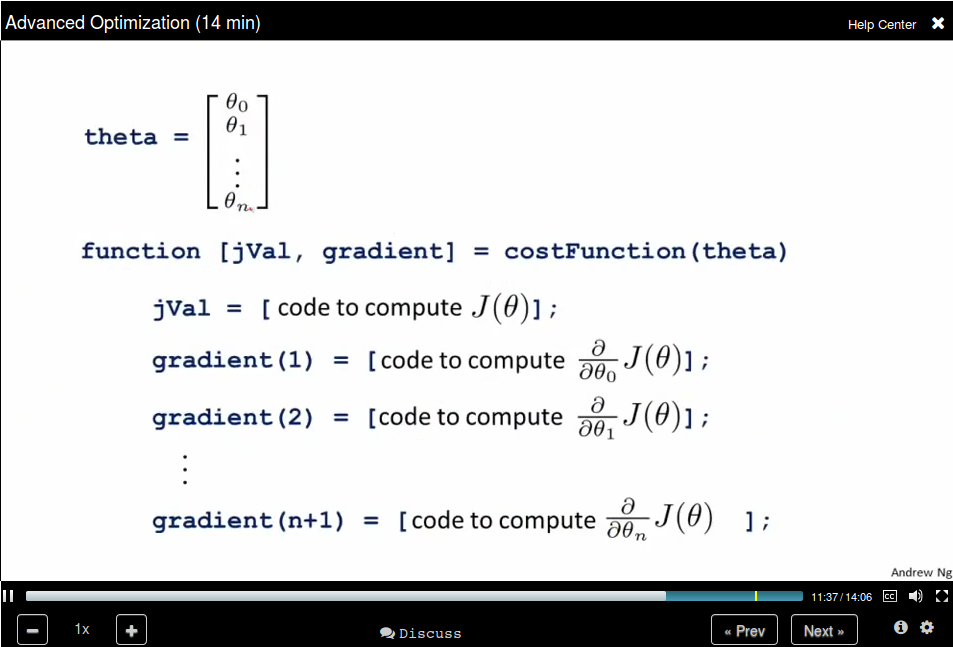

Advance Optimization

Note that the Octave start from 1 instead of 0.

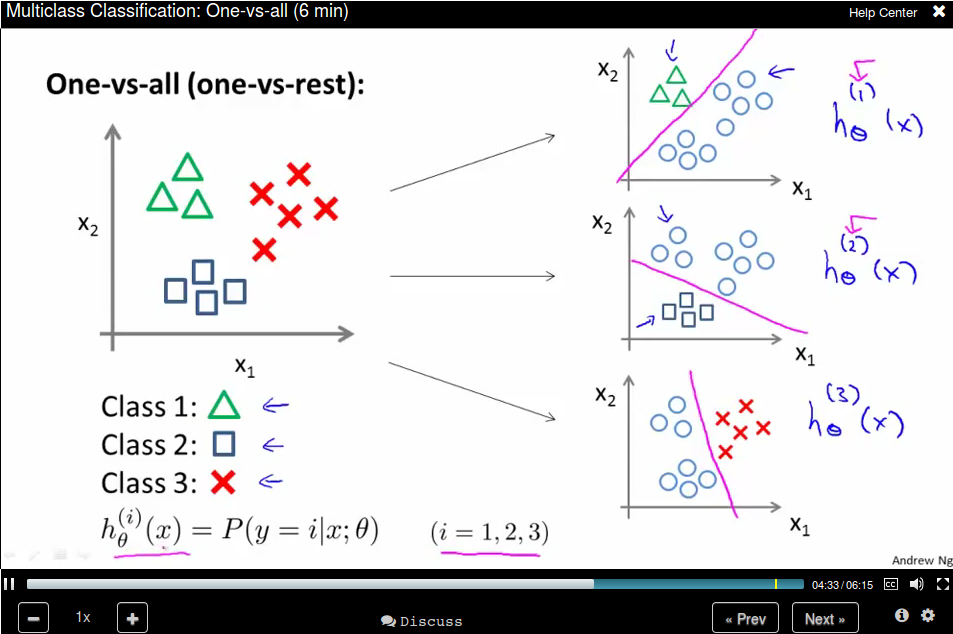

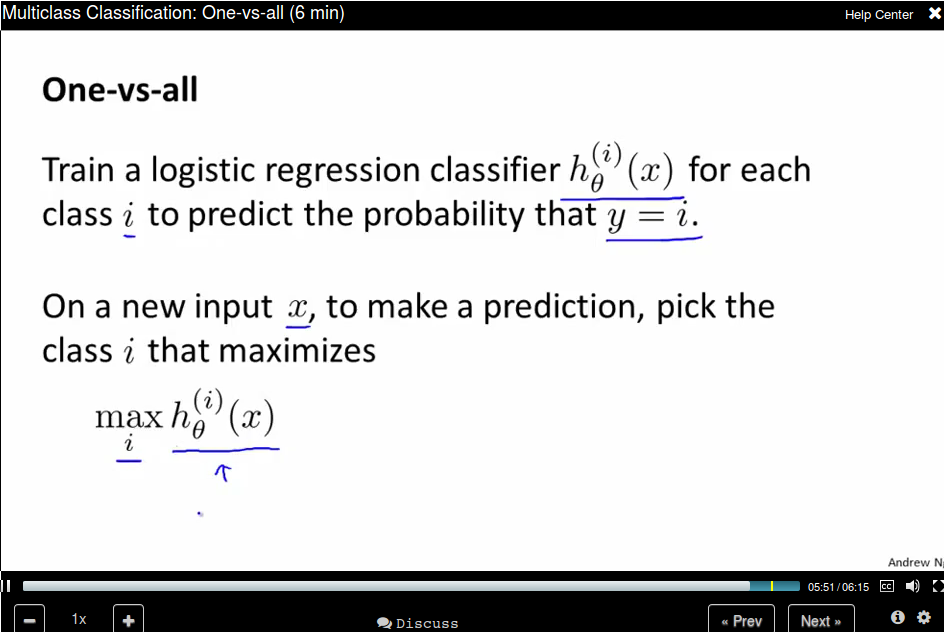

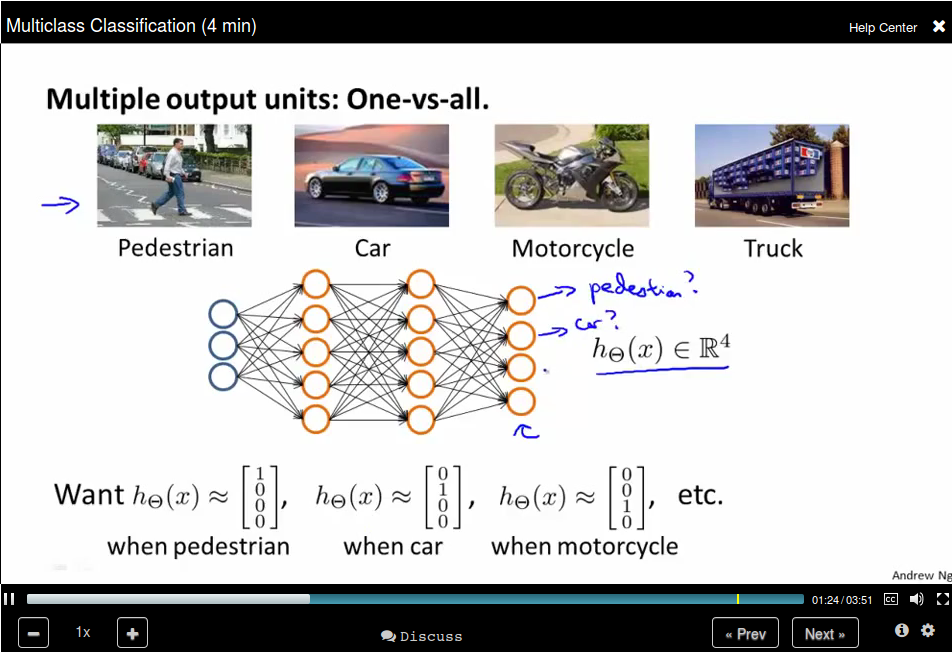

Multiclass Classification: One-vs-all

One-vs-all is also called one-vs-rest.

The method is:

Regulation (Week 3)

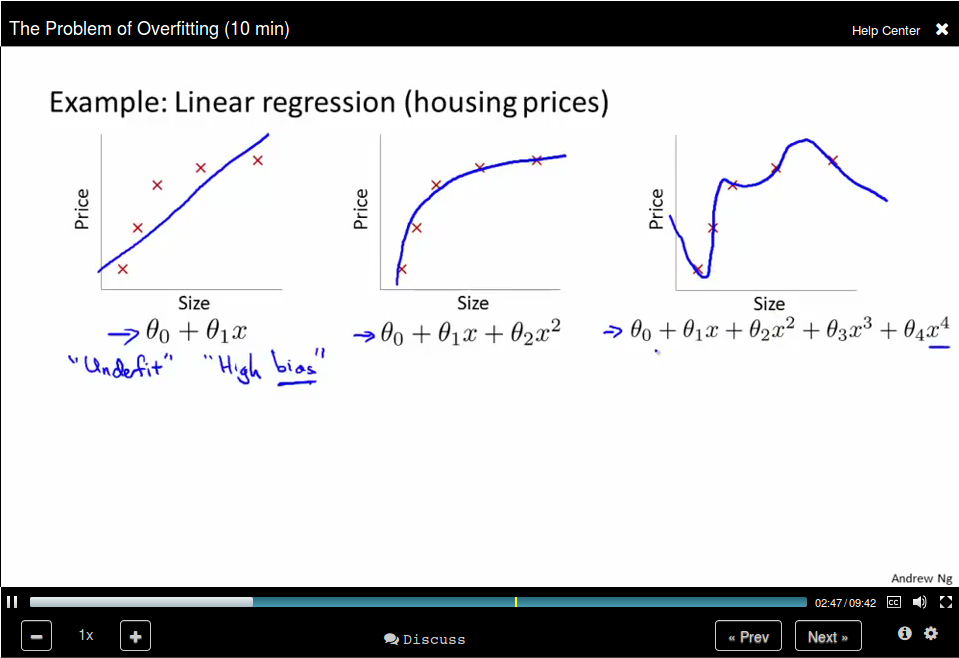

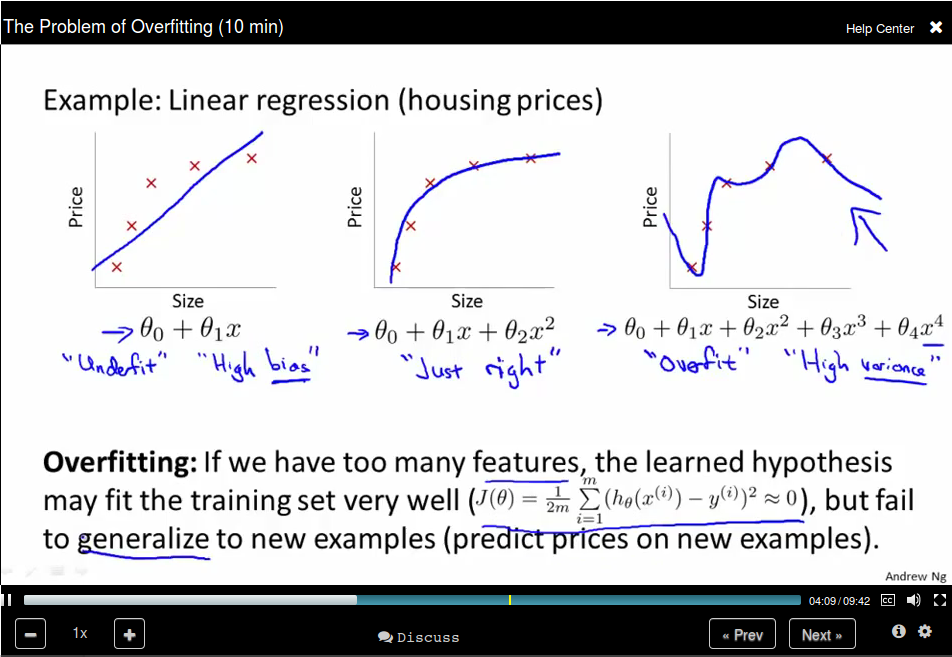

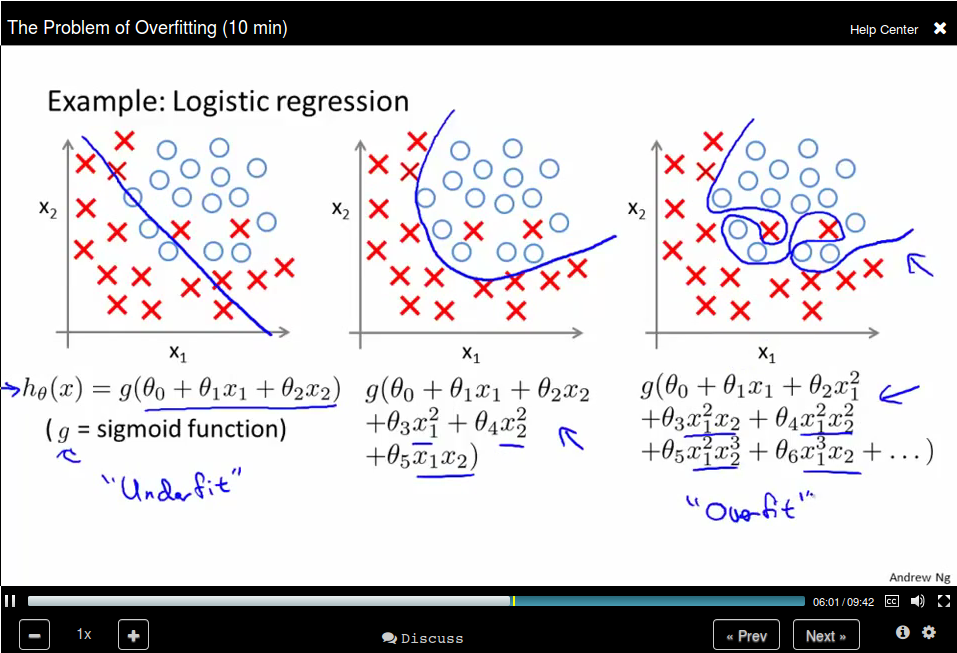

The problem of Overfitting

For Logistic regression:

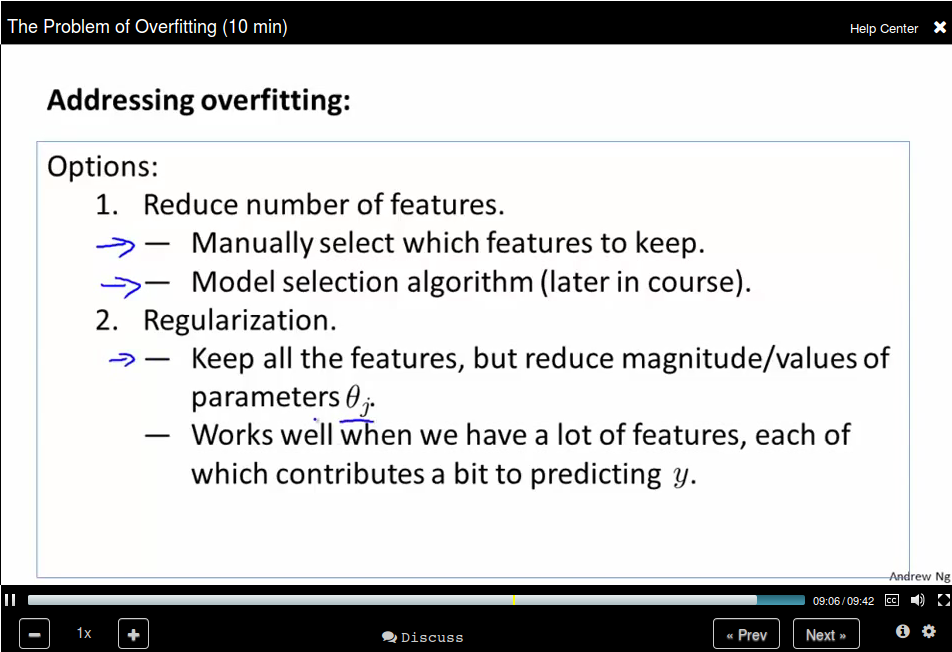

How to solve the problem?

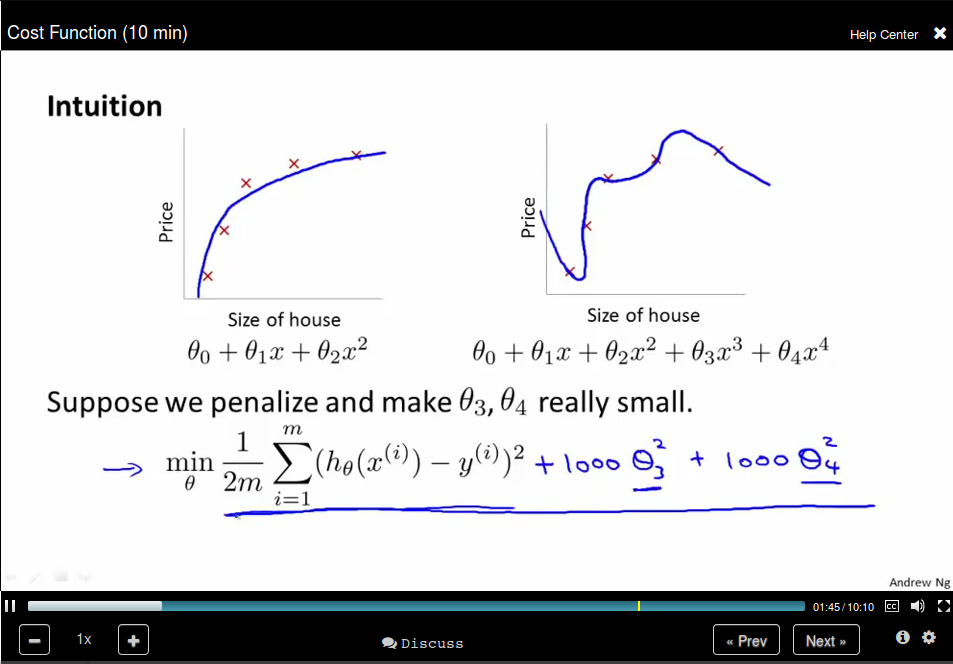

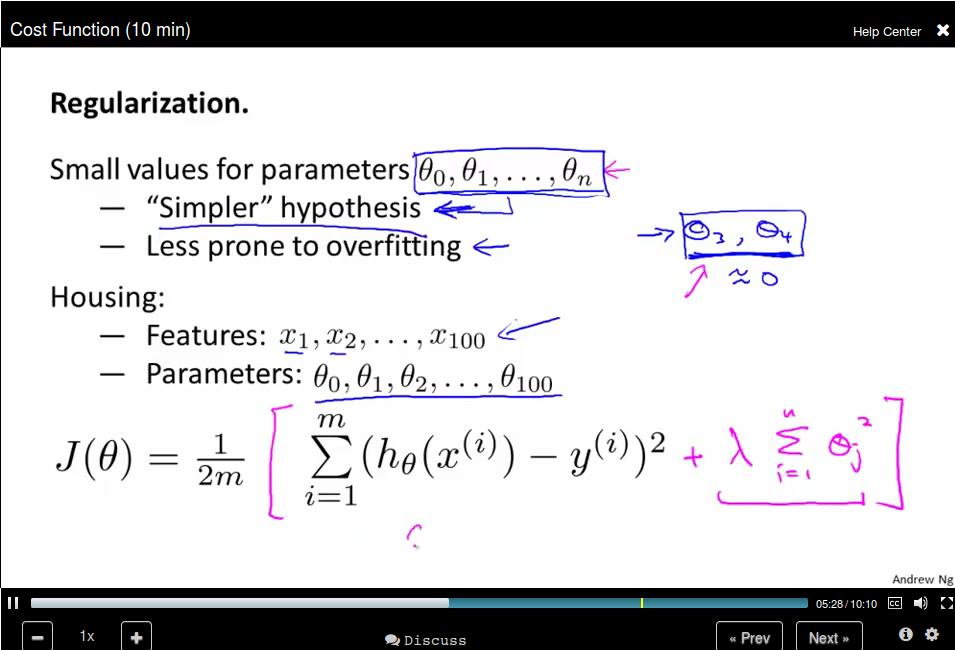

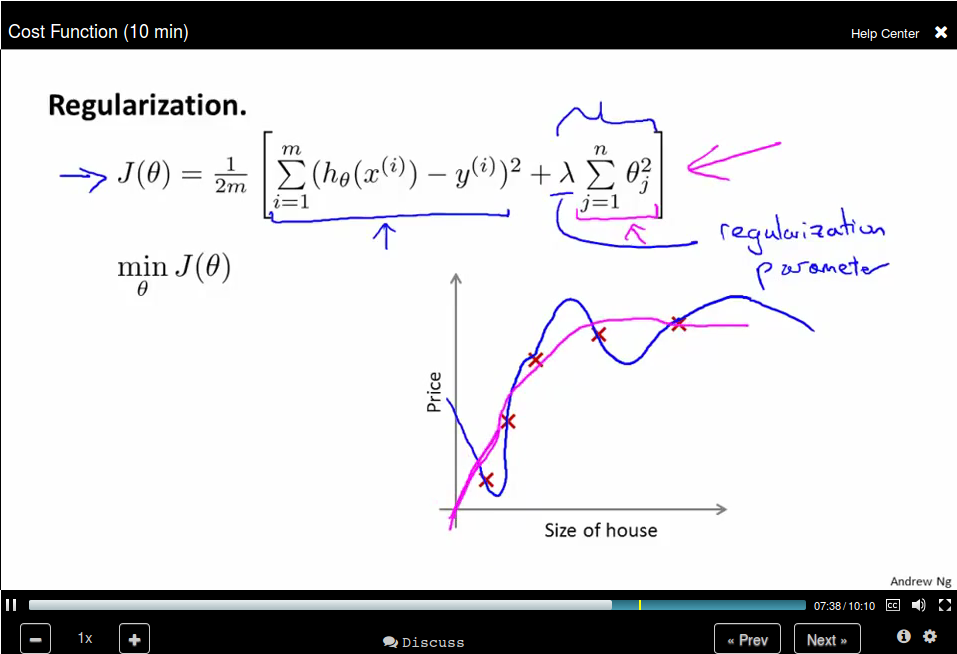

Cost Function

The idea behind regulation is that:

The idea behind regulation is that:

Note that we didn't penalize θ_0

Note that we didn't penalize θ_0

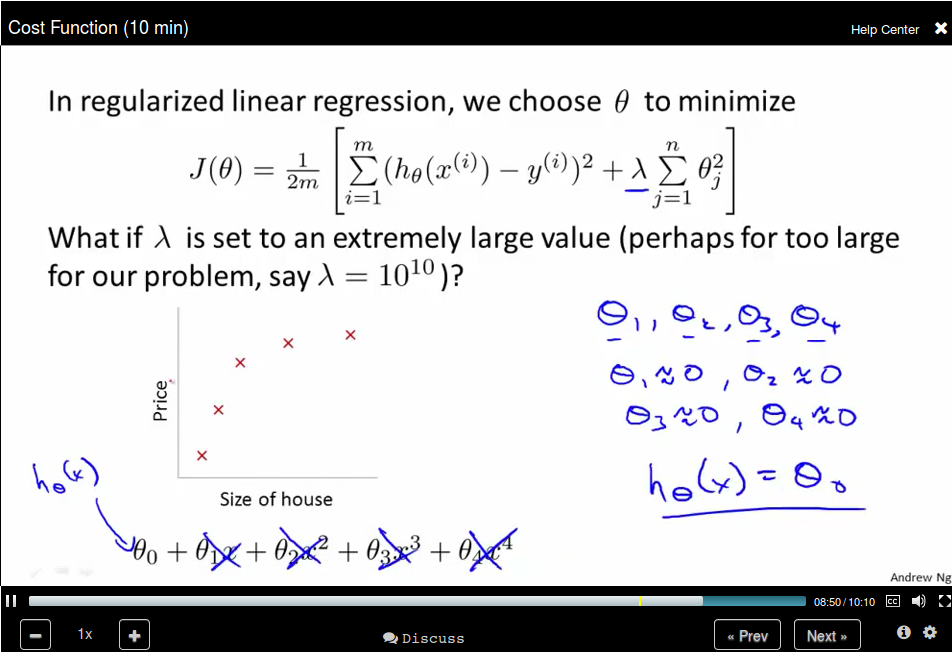

What if λ is too large?

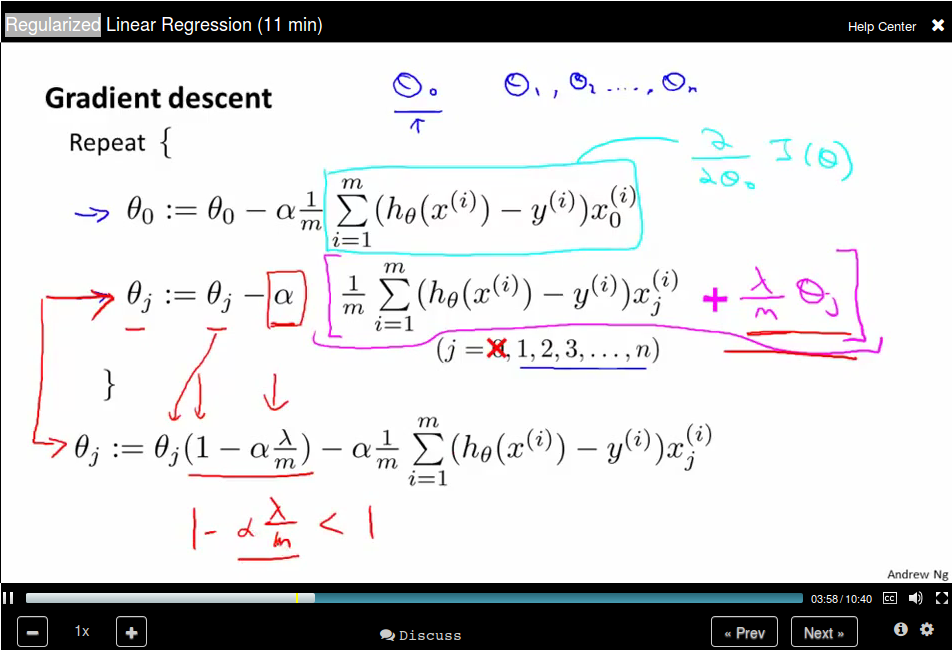

Regularized linear regression

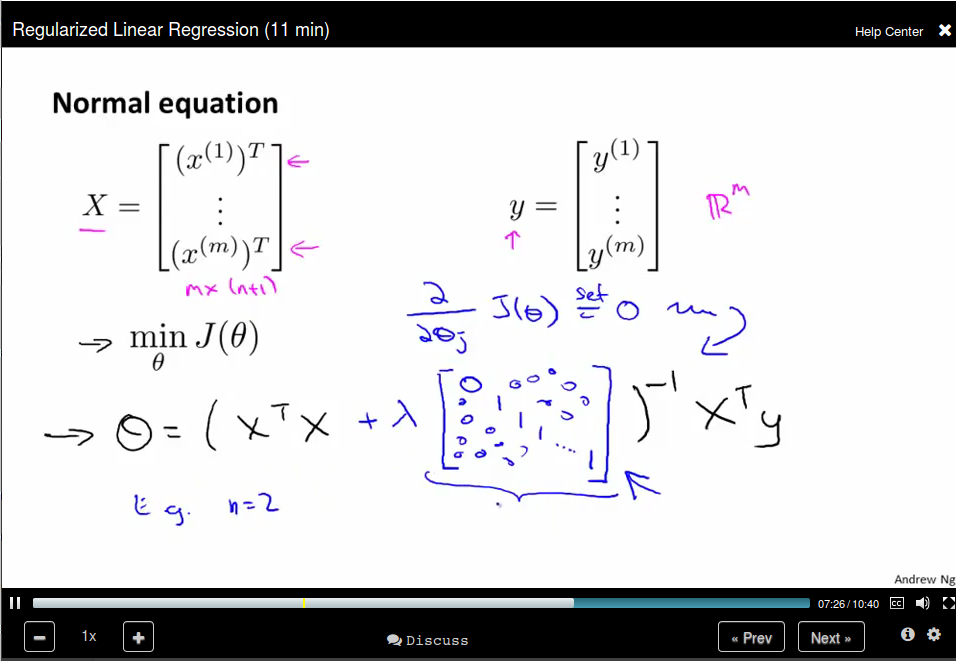

When using normal equation:

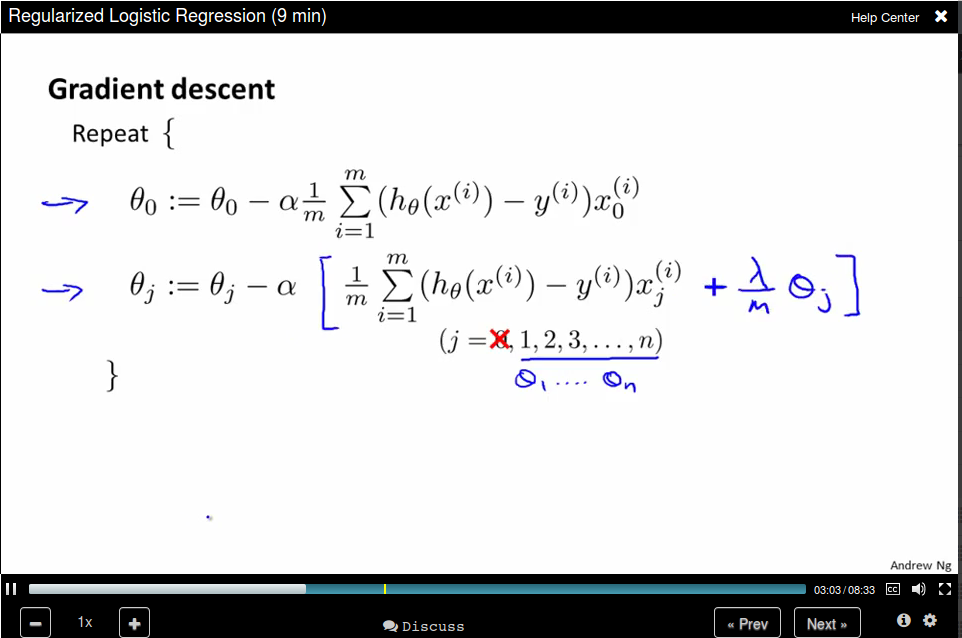

Regularized Logistic Regression

Now update θ_0 separately

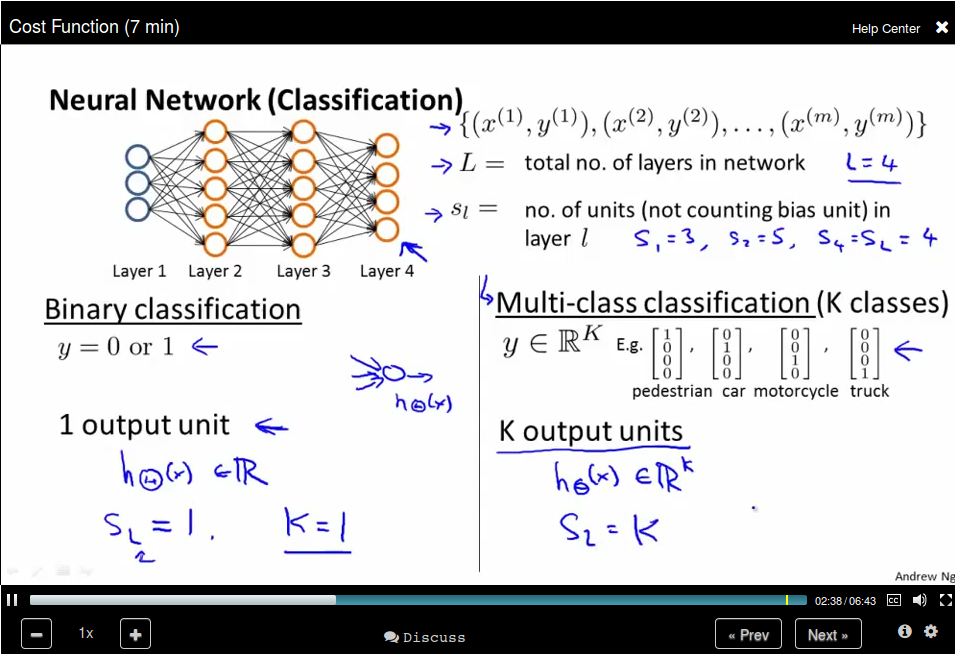

Neural Networks: Representation

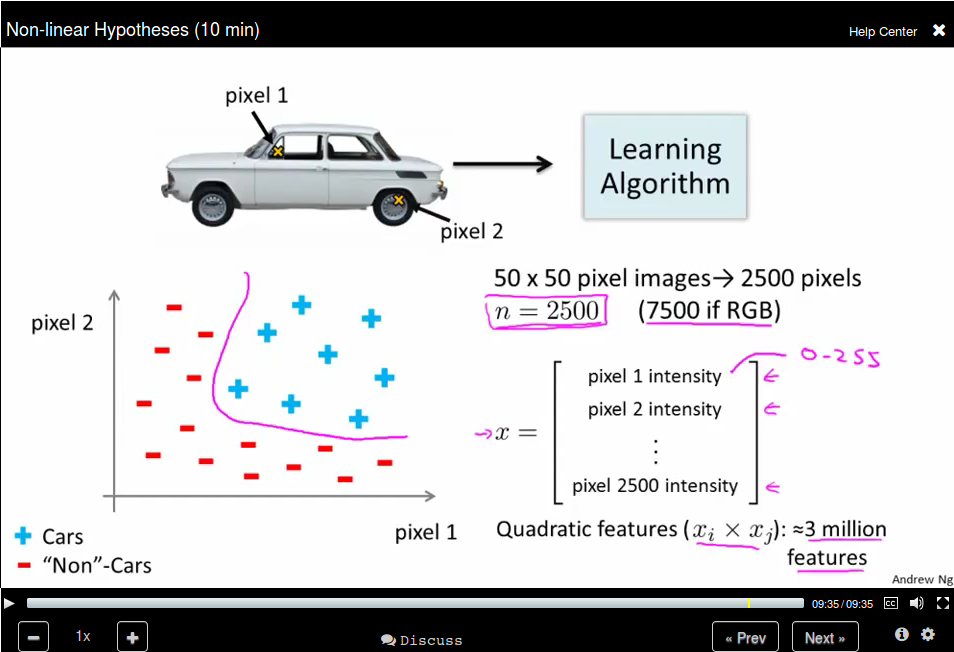

Non-linear Hypotheses

Use quadratic features will results in a lot of features.

Neurons and the Brain

There is one learning algorithm of the brain

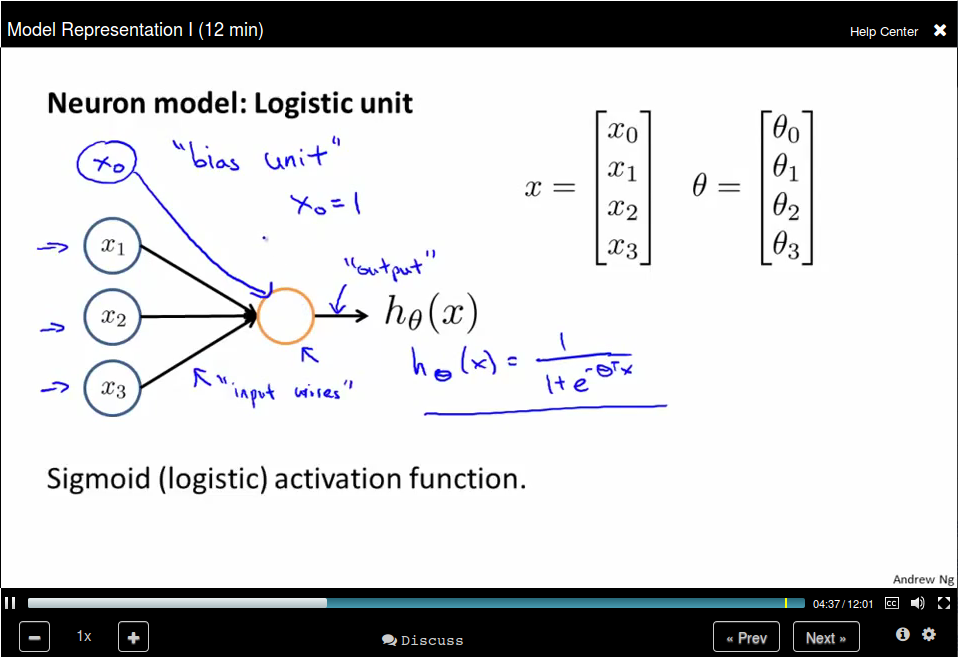

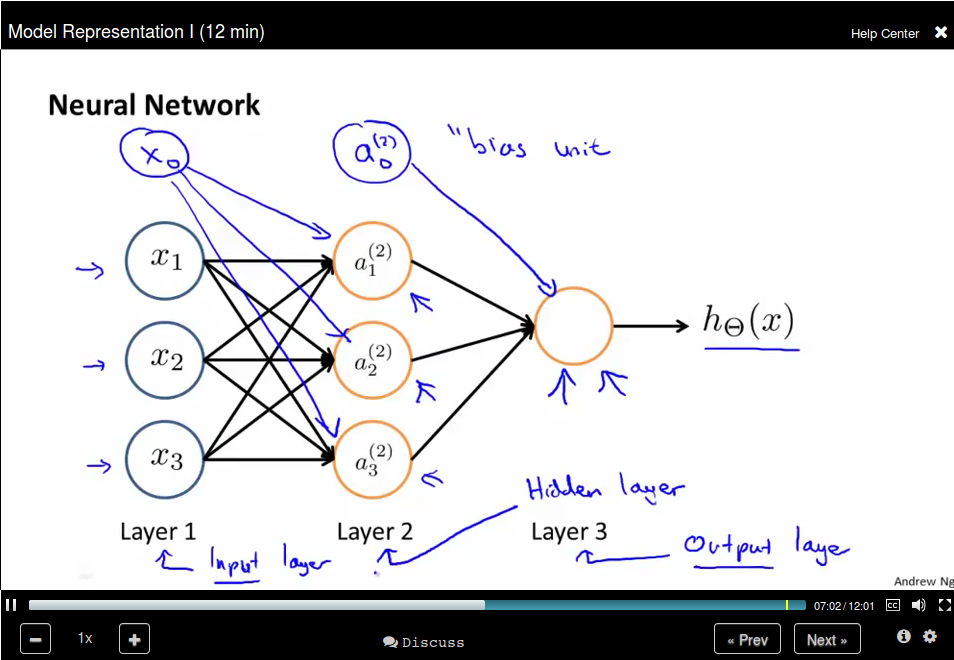

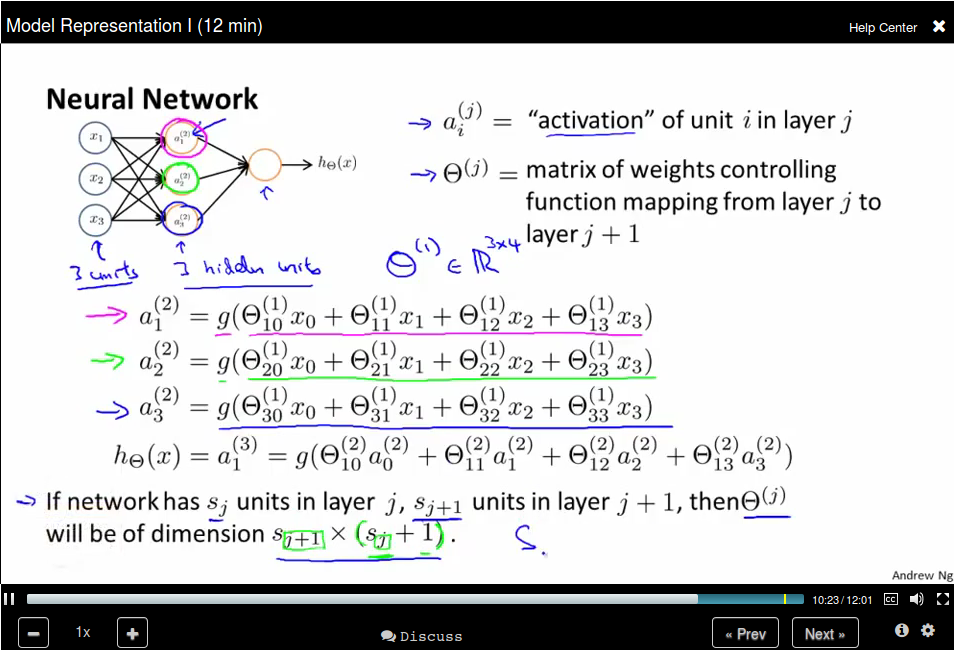

Model Representation I

Neuron model: Logistic unit

Neural Network is a group of this neural.

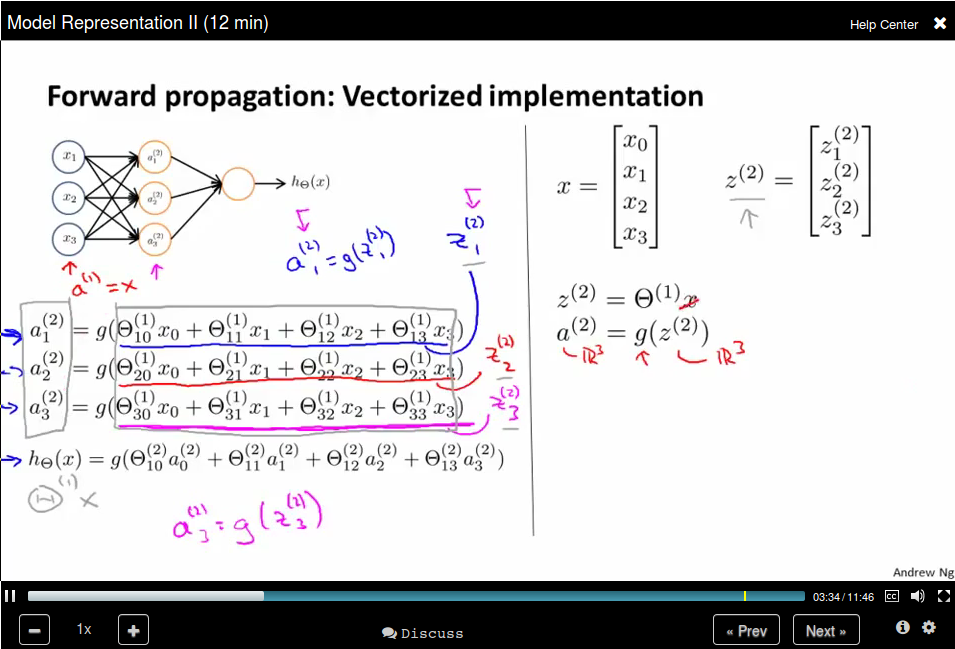

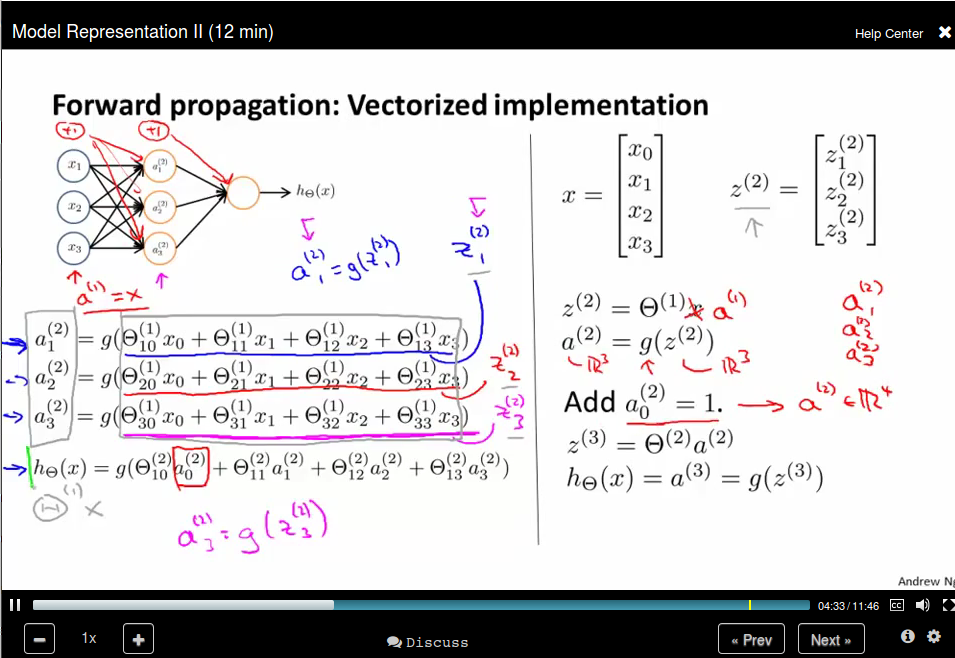

Model Representation II

Forward propagation: Vectorized implementation

Bias unit:

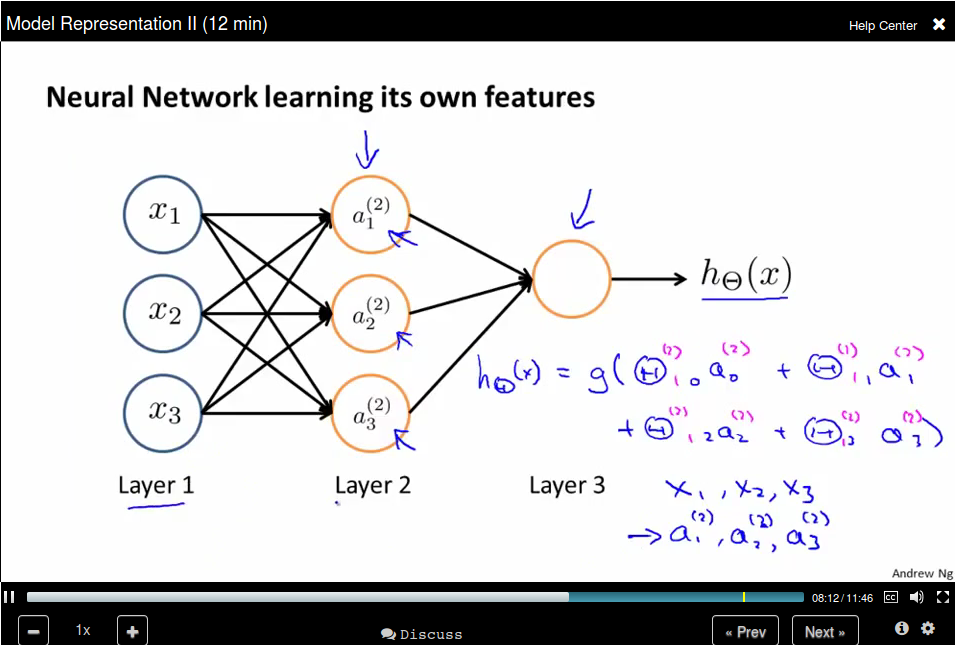

The last layer is like Logistic Regression, but Neural Network learning its own

features.

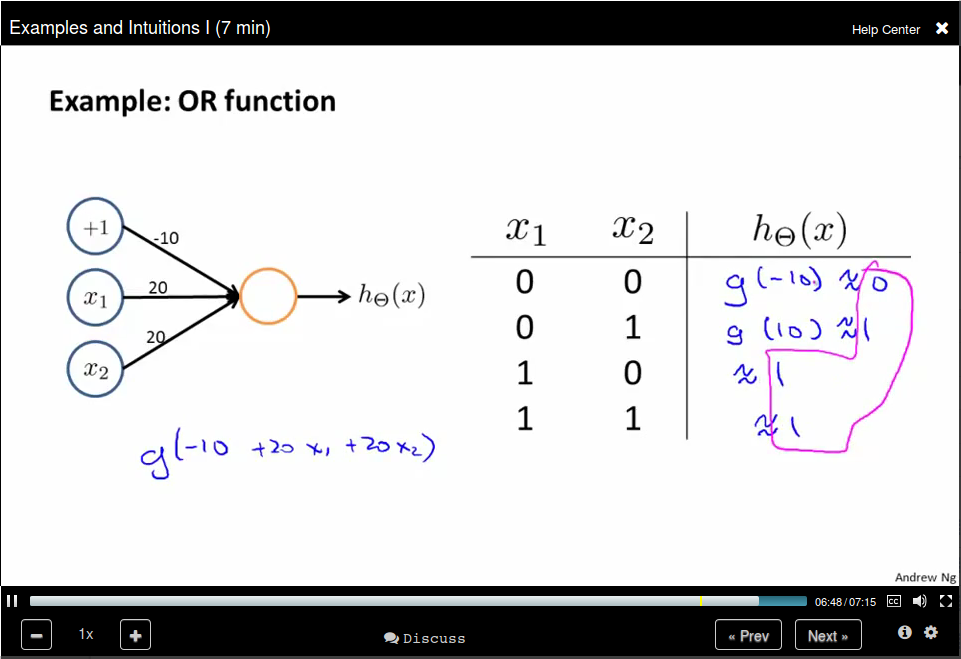

Examples and Intuitions I

OR Function

Examples and Intuitions II

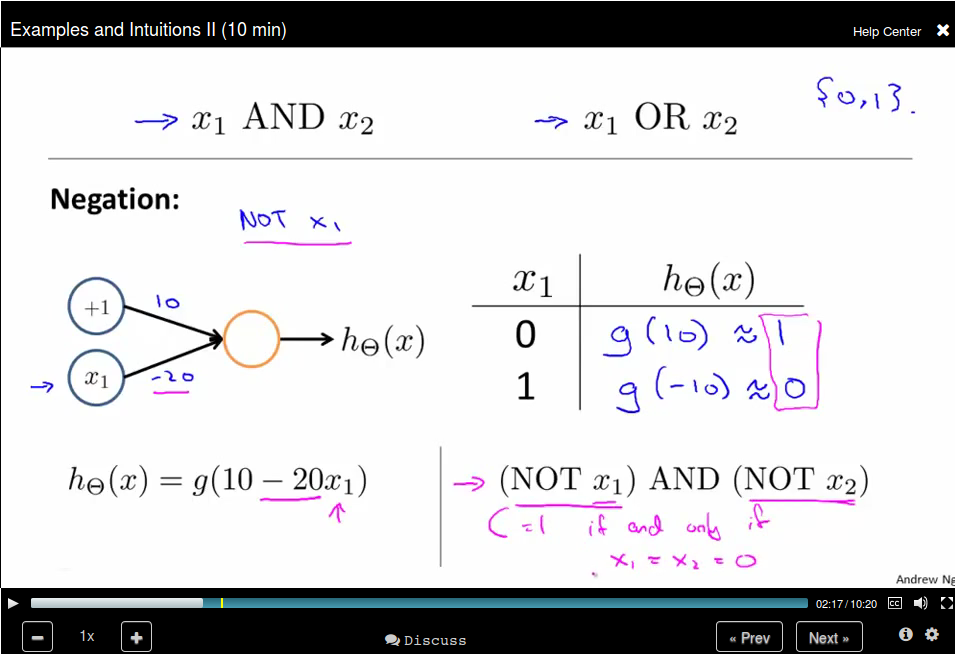

NOT Function

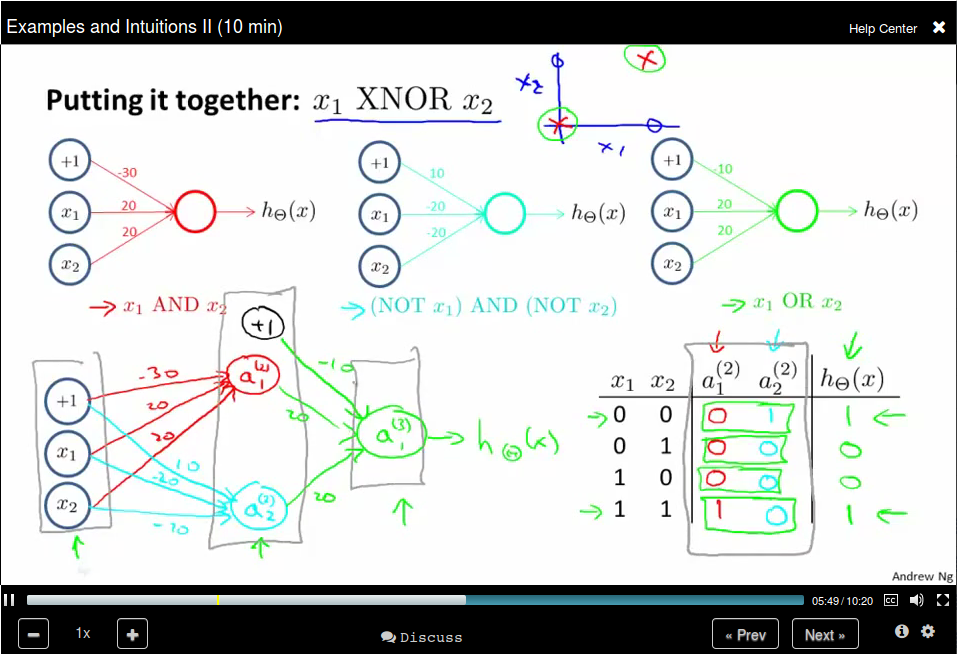

The input layer has only x_1 and x_2. The second layer compute the feature (x_1 AND x_2), and the feature (NOT x_1) AND (NOT x_2). The third layer use the feature computed in layer 2 and do an OR operation to simulates a XNOR operation.

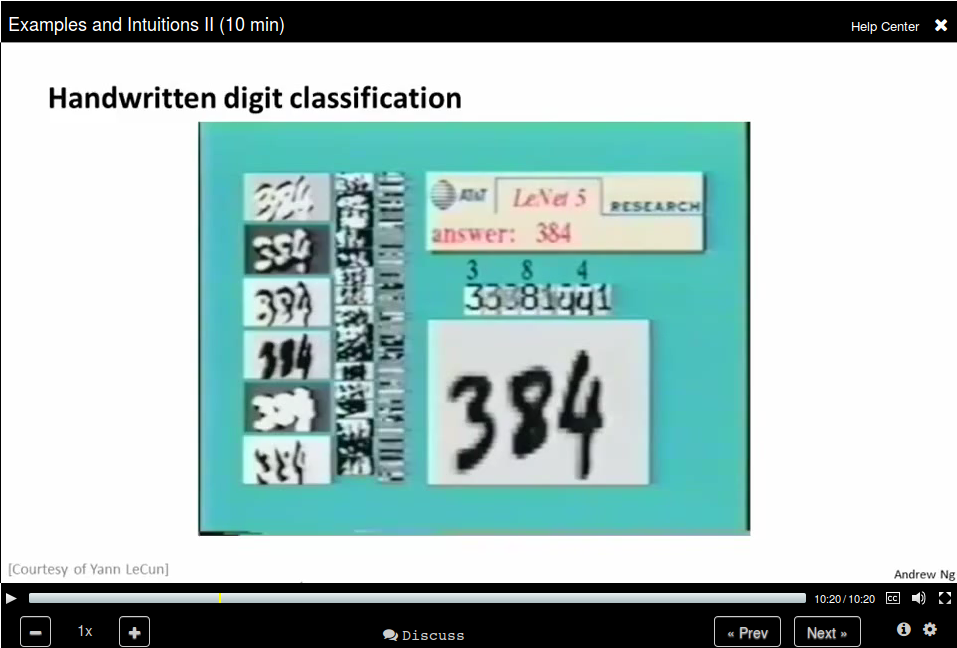

Handwritten digit classification

Mutilcass Classification

Use an extension of the One-vs-all method.

Neural Networks: Learning (Week 5)

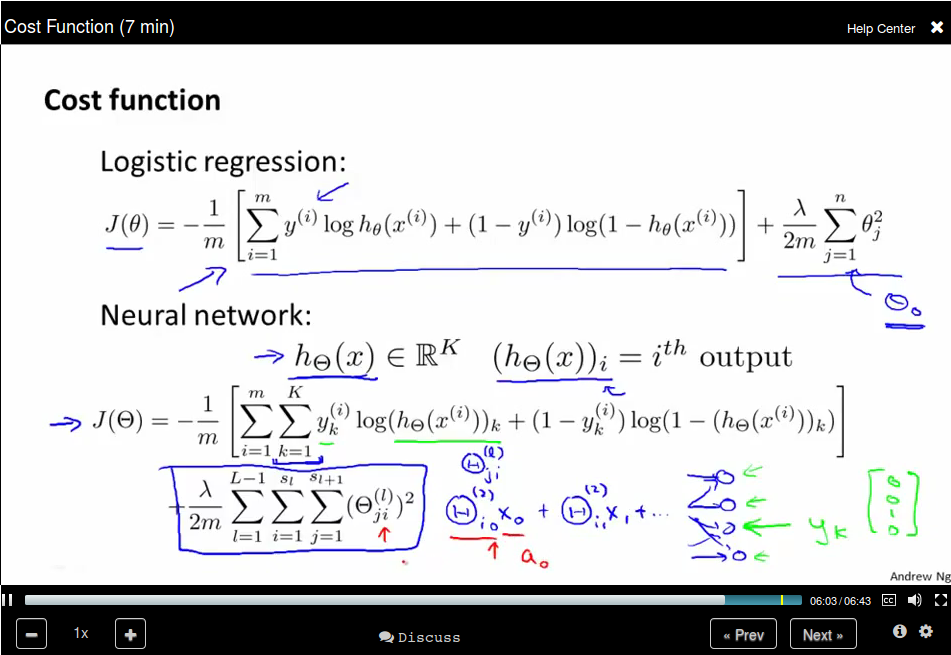

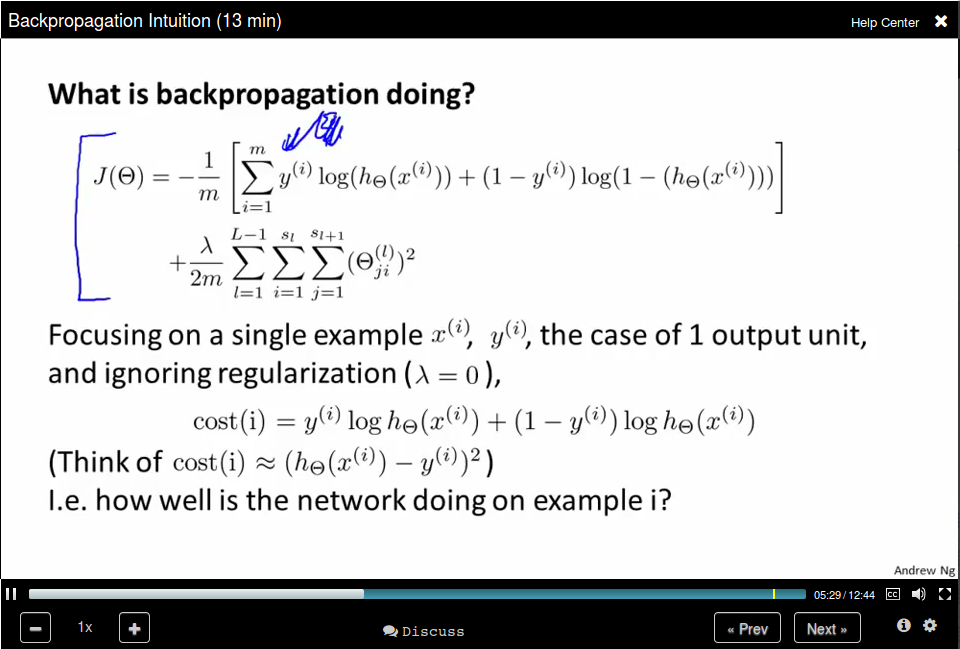

Cost Function

This is the cost function

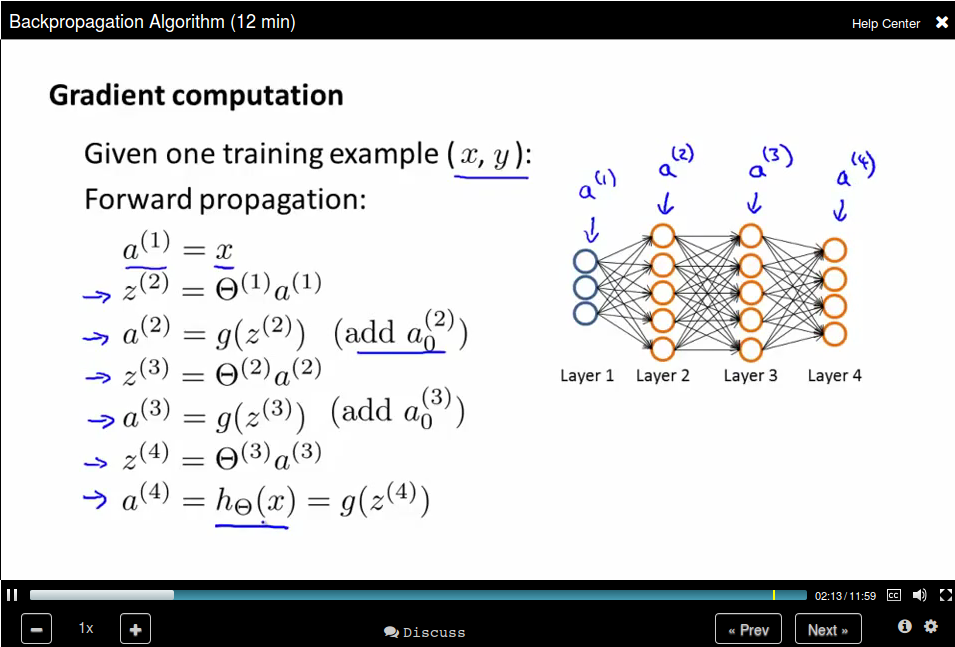

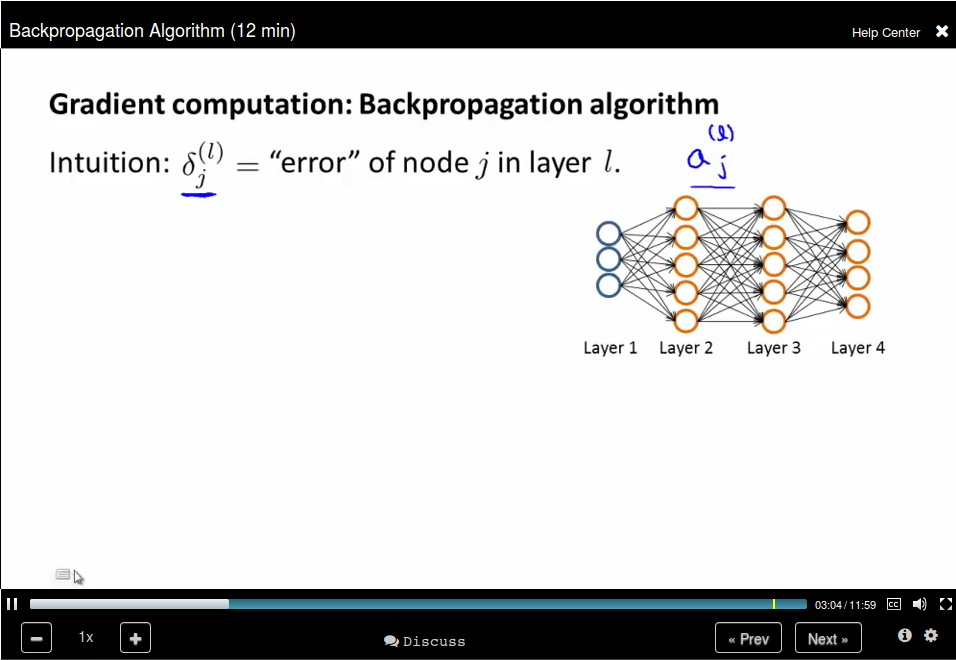

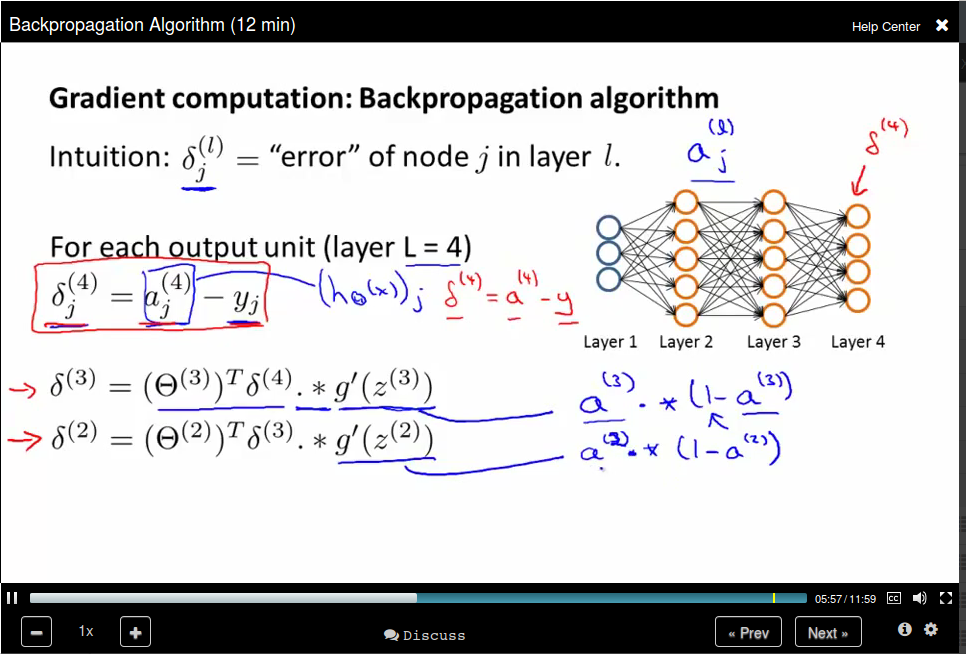

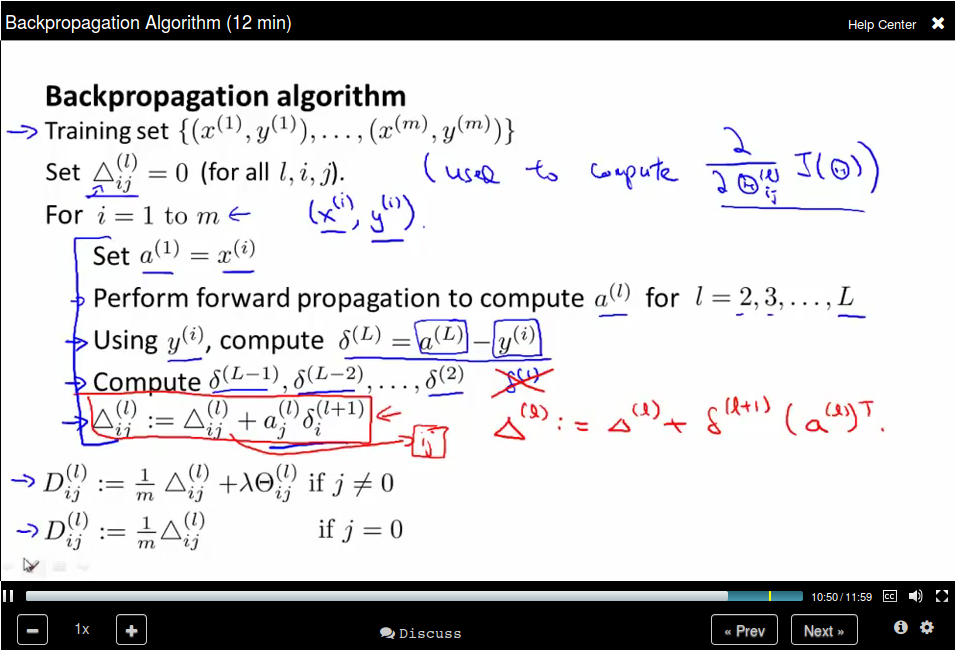

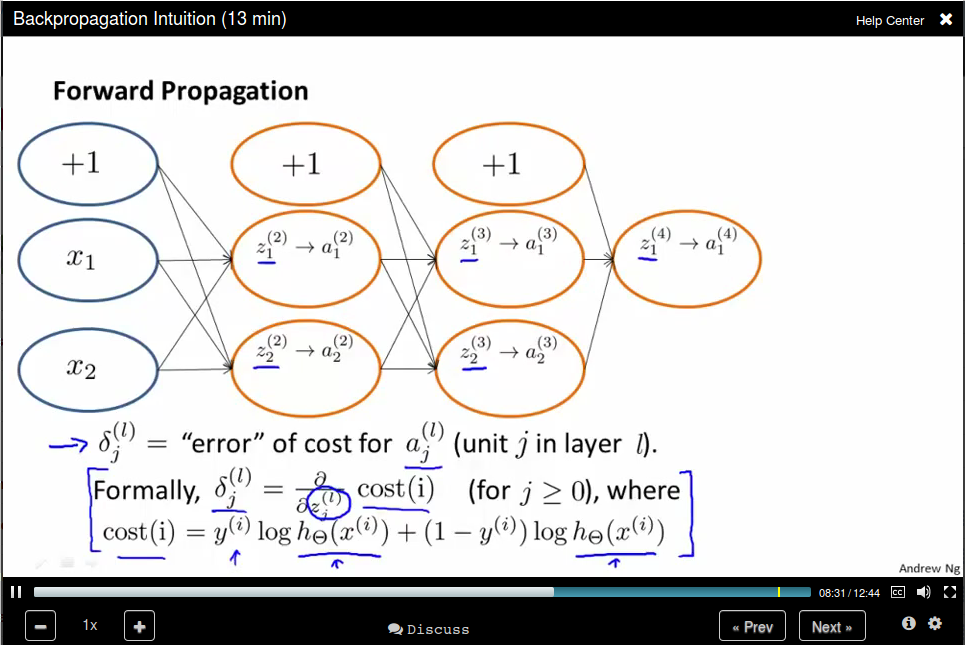

Backpropagation Algorithm

Forward Propagation, computing all the activations:

Backpropagation algorithm, computing the gradient:

The name "back" comes from the order we compute the "error"

Backpropagation algorithm

Backpropagation Intuition

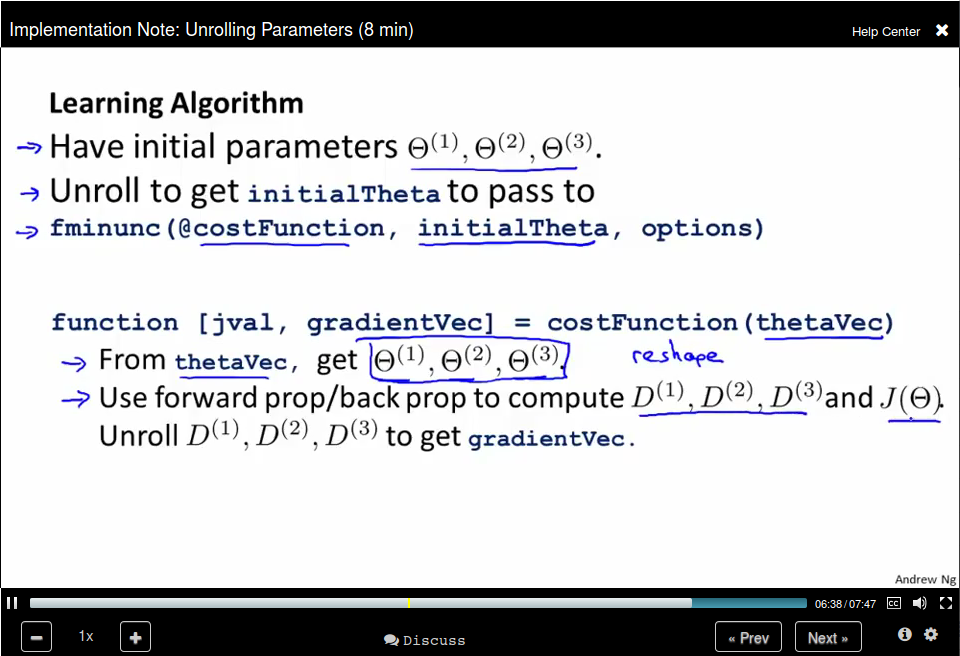

Implementation Notes Unrolling Parameters

In Neural Network our parameters are matrices, and we need to unroll it into vectors.

Gradient Checking

Use nummerical estimation of gradients to check.

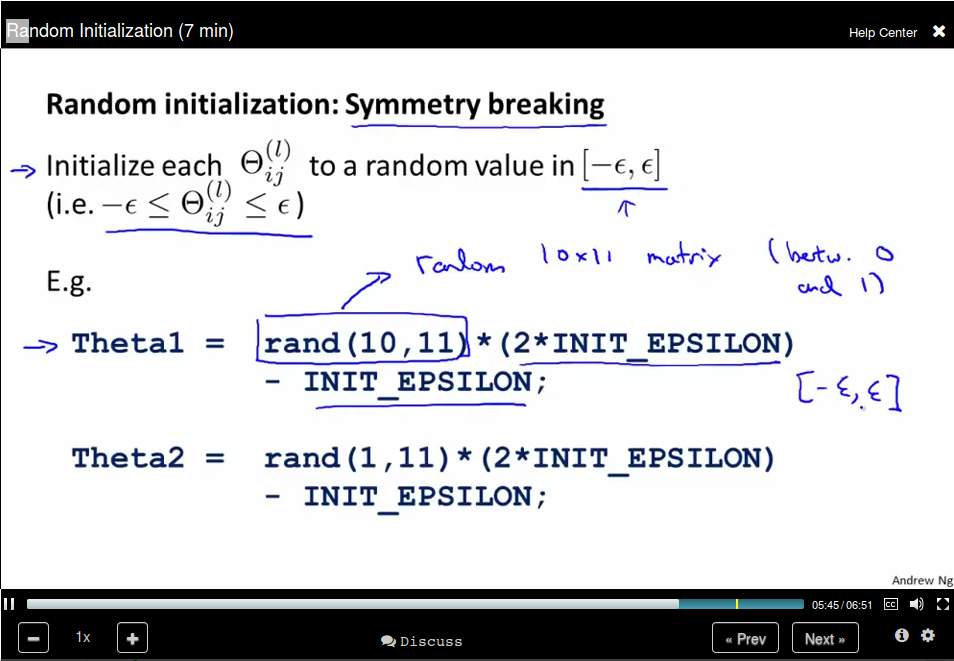

Random Initialization

We need to provide an initial value for gradient fescent and advanced optimization method.

Zero Initialization will result in identical values.

To solve this problem, we use random initialization to break the symmerty.

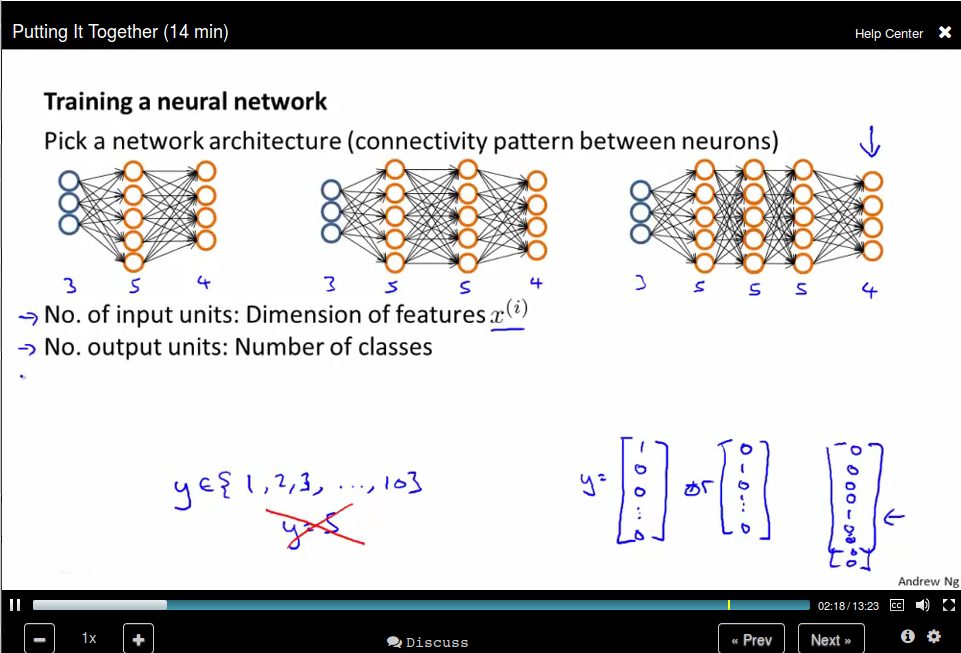

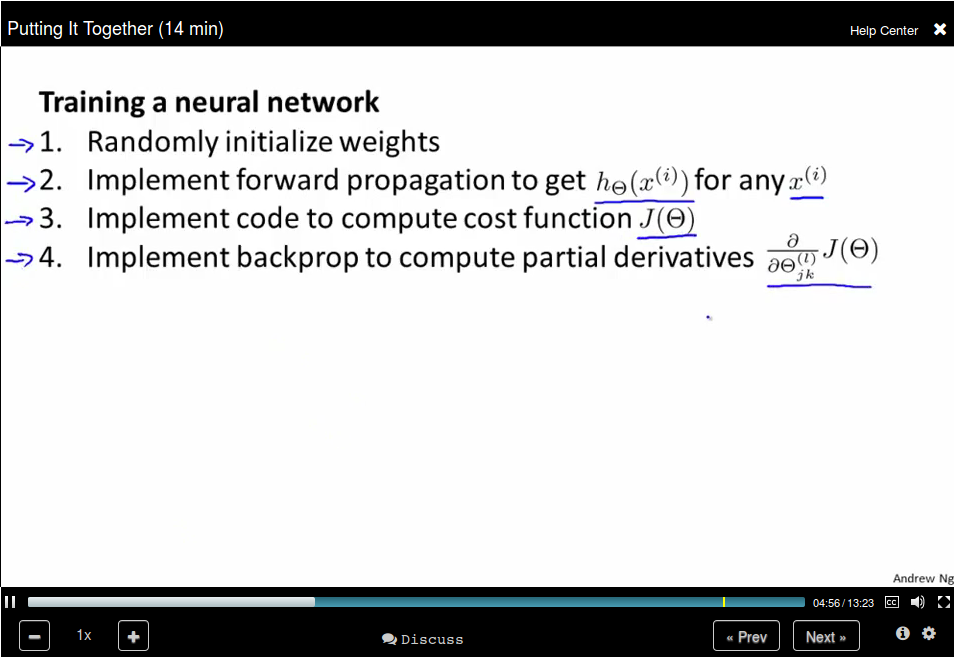

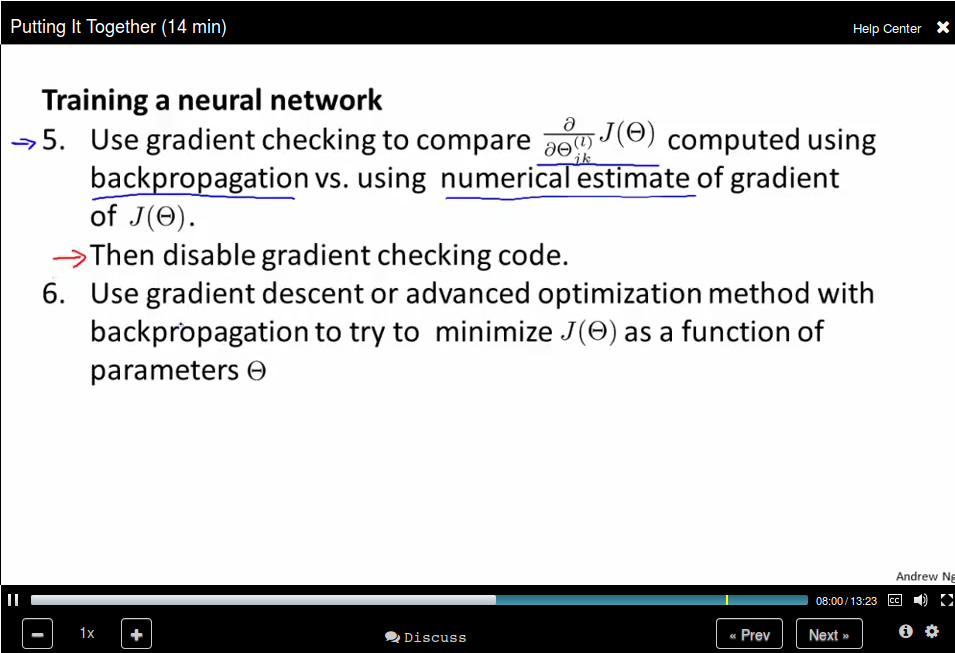

Put it together

How to train a neural network

Advice for Applying machine Learning

Deciding What to Try Next

- Get more training examples

- Try smaller sets of features

- Try getting additional features.

- Try adding polynomial features

- Try decreasing λ.

- Try increasing λ.

Evaluating a Hypothesis

Hypothesis can be overfitting.

We can evaluate our hypothesis by separate our date into training set and test set.

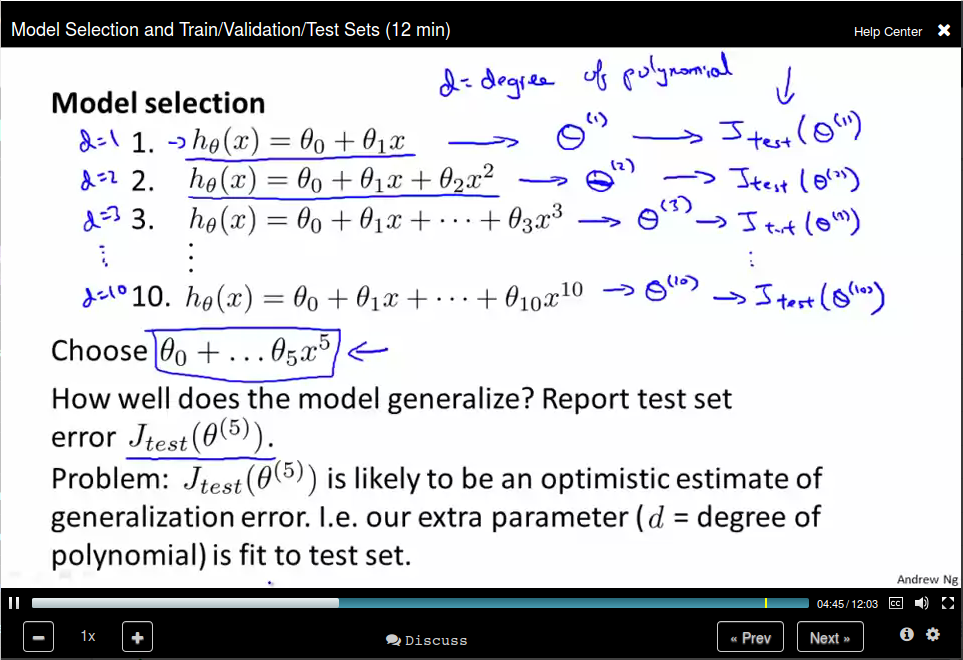

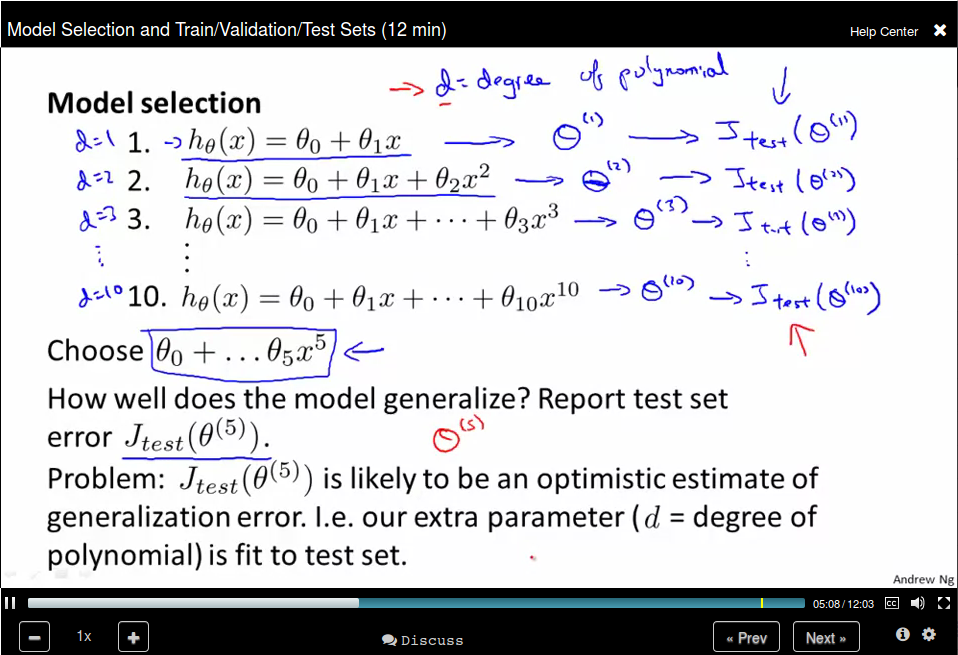

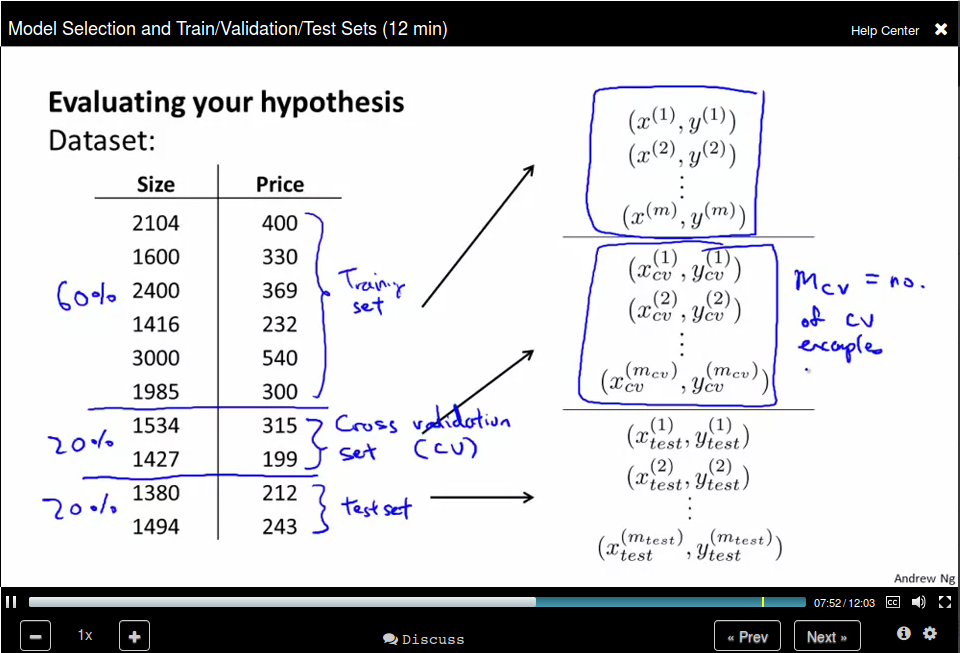

Model Selection and Train/Validation/Test Sets

To address this problem, we divide our data set into three parts: training set, cross validation set, and test set.

To address this problem, we divide our data set into three parts: training set, cross validation set, and test set.

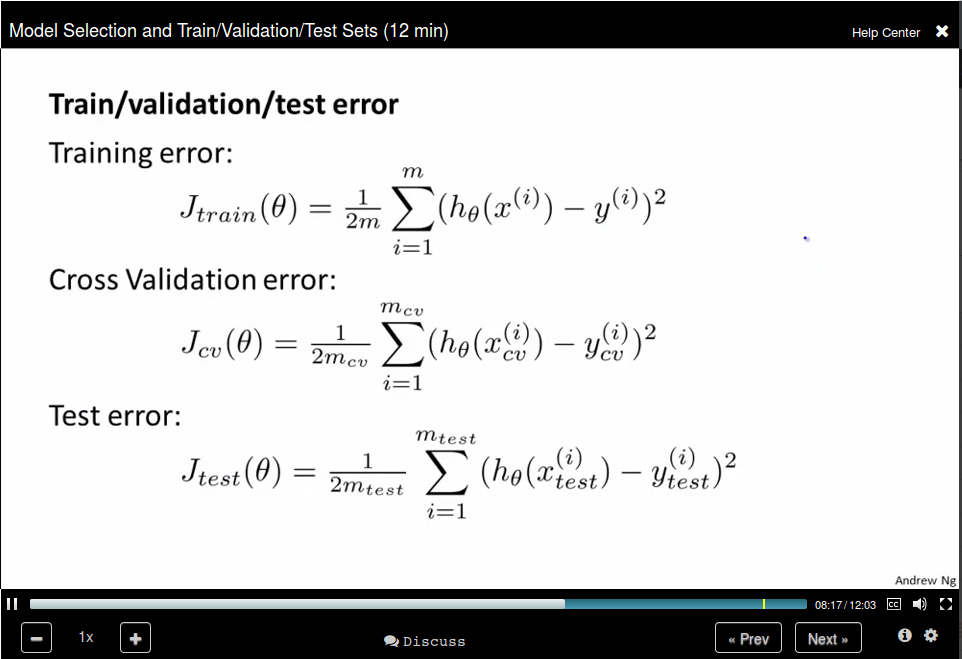

Use cross validation error to selection the model degree and use test set error to select θ.

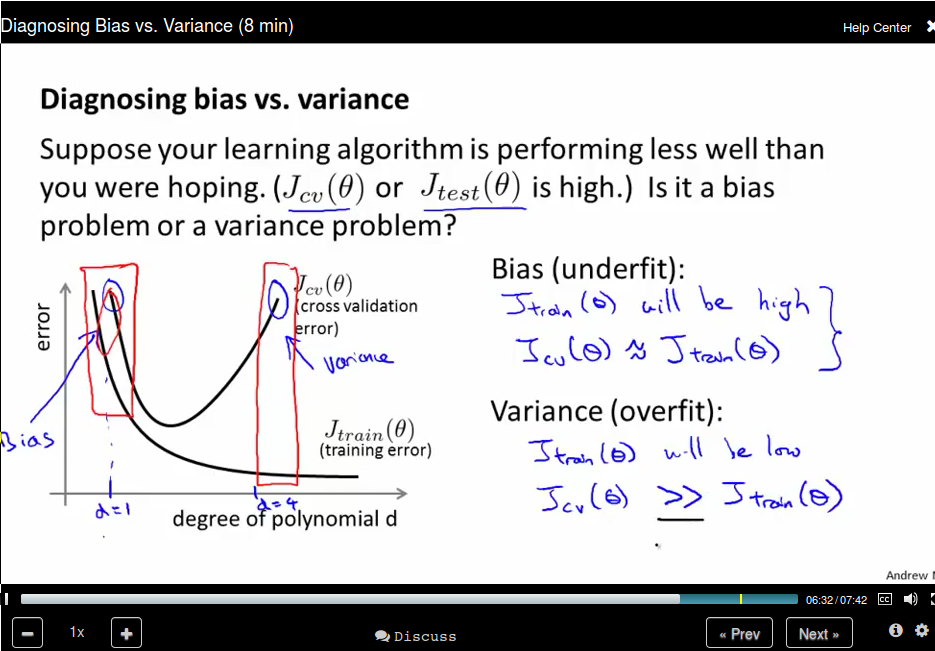

Diagonosing Bias vs Variance

Bias (undearfit)

Variance (overfit)